Exploratory Factor Analysis

Exploratory Factor analysis

Some resources:

Libraries used:

psychGPArotationfactoextra

PCA and SVD are considered simple forms of exploratory factor analysis. The term ‘factor analysis’ is a bit confusing and you will find a variety of definitions out there–some people assert that PCA is not factor analysis, and others might use PCA but call it factor analysis. Remember that PCA involves a complete redescription of the covariance or correlation matrix along a set of independent dimensions using Eigen decomposition, until they completely redescribe the data. Eigen decomposition ranks the dimensions by the variance, and so there is a fall-off in how useful consecutive dimensions are. We usually pick off the most important components and ignore the rest, treating them as noise. But if we think about what we learned with cluster analysis and MDS, sometimes there are unique but important low-level aspects of variance that might be better to incorporate into our components. MDS does this by forcing the distance space into a fixed number of dimensions. Similarly, factor analysis tries to fit a model of a fixed number of dimensions or factors. It does this by trying to maximize the variance accounted for by a fixed number of ‘latent’ factors, so that we have a deliberate model + error approach. In any case, like PCA factor analysis involves modeling the covariance or correlation matrix, and is an example of a broader set of approaches called ‘covariance models’.

Making an analogy to MDS, classic MDS used eigen decomposition and then peels off just the top dimensions. But sammon and non-metric scaling try to force the higher dimensions into fewer. Now, instead of fitting all the noise, we can minimize or optimize some notion of fitting the correlation matrix, and treat everything else as noise. When an algorithm has this goal, it is typically called ‘factor analysis’. As such, it is important when you report an analysis to give specific details of how the analysis was performed, including the software routine and arguments used.

A simple example

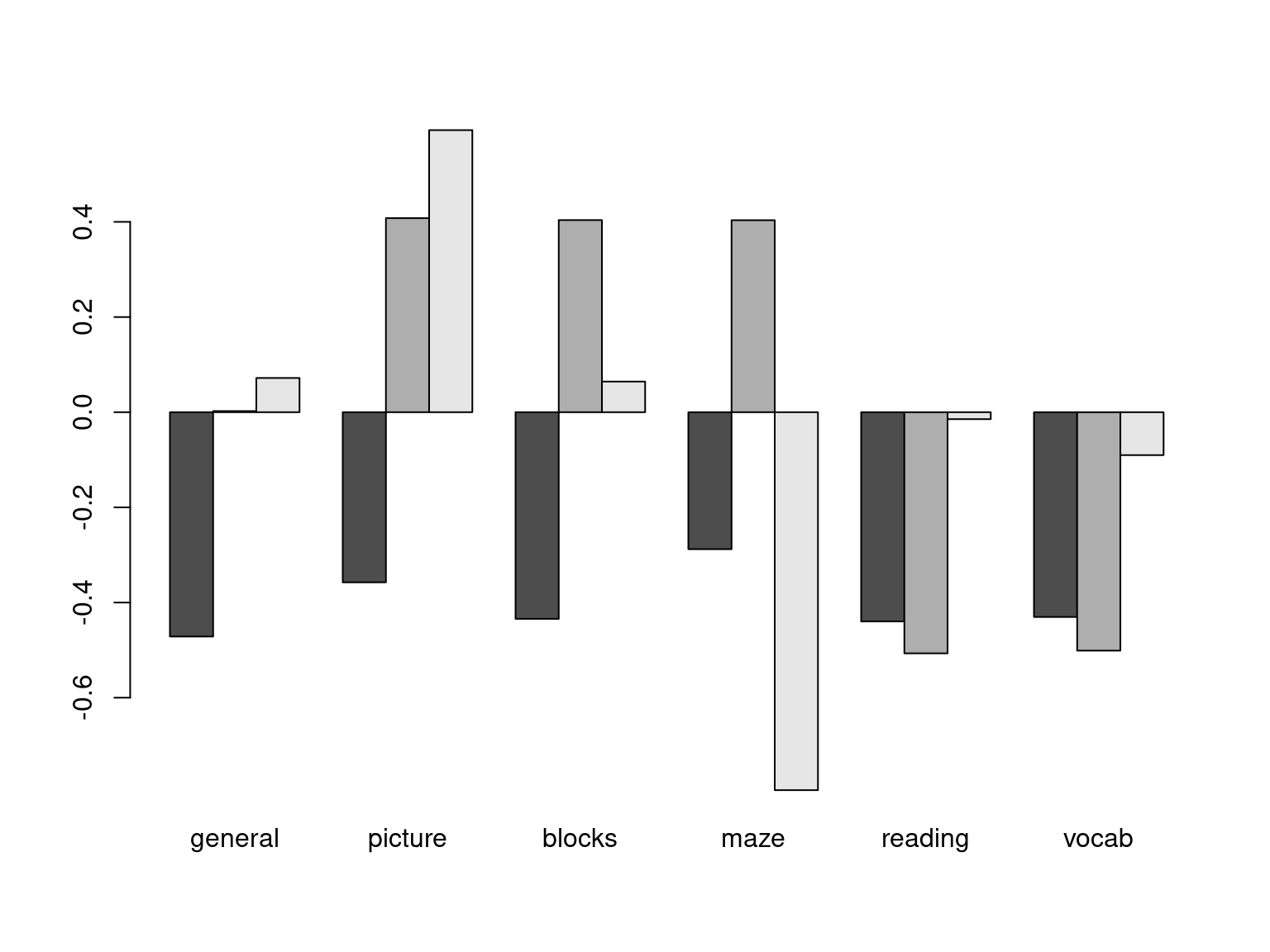

In the section on PCA, we examined human abilities and came up with a solution in which one component was an overall ability across all skills, one was visual vs. verbal, and a third was picture vs. maze:

library(GPArotation)

# library(psych)

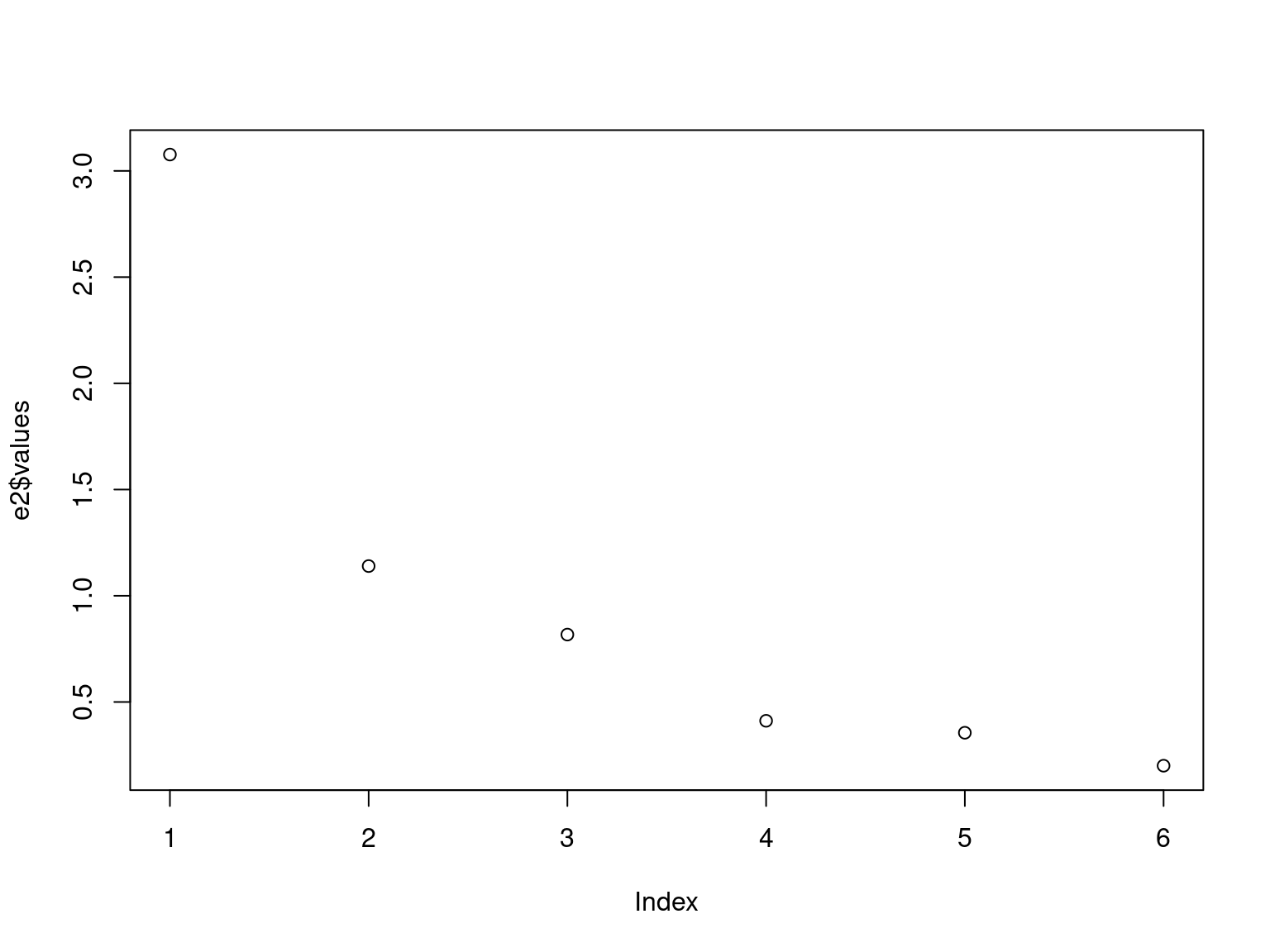

data(ability.cov)

e2 <- eigen(cov2cor(ability.cov$cov))

plot(e2$values)

[,1] [,2] [,3] [,4] [,5] [,6]

general -0.471 0.002 0.072 0.863 0.037 -0.164

picture -0.358 0.408 0.593 -0.268 0.531 0.002

blocks -0.434 0.404 0.064 -0.201 -0.775 0.051

maze -0.288 0.404 -0.794 -0.097 0.334 0.052

reading -0.440 -0.507 -0.015 -0.100 0.056 0.733

vocab -0.430 -0.501 -0.090 -0.352 0.021 -0.657

We can use the factanal function to do something

similar, giving it the covariance matrix. We now specify exactly how

many factors we want:

Call:

factanal(factors = 3, covmat = ability.cov)

Uniquenesses:

general picture blocks maze reading vocab

0.441 0.217 0.329 0.580 0.040 0.336

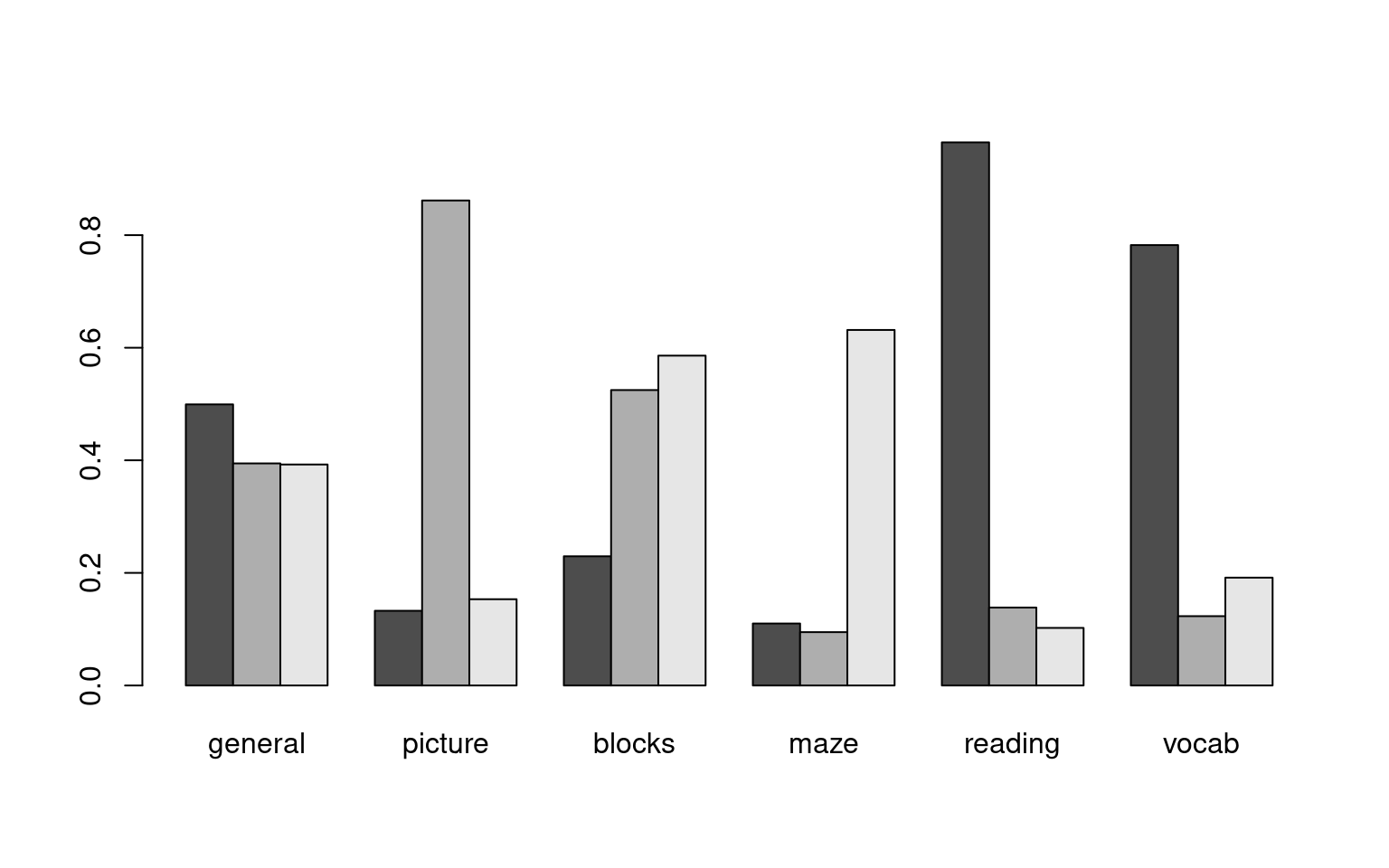

Loadings:

Factor1 Factor2 Factor3

general 0.499 0.394 0.393

picture 0.133 0.862 0.153

blocks 0.230 0.525 0.586

maze 0.110 0.632

reading 0.965 0.138 0.102

vocab 0.782 0.123 0.192

Factor1 Factor2 Factor3

SS loadings 1.874 1.217 0.967

Proportion Var 0.312 0.203 0.161

Cumulative Var 0.312 0.515 0.676

The degrees of freedom for the model is 0 and the fit was 0  Now, the first three factors turn out a bit differently. factor1 is the

specific

Now, the first three factors turn out a bit differently. factor1 is the

specific general skill, reading and vocab–a basic verbal

ability. Factor 2 is picture+books; the visual skills that don’t involve

maze, plus some general. The third loads highly on blocks, maze, and

general. These tend to focus on single common positively-correlated

factors rather than the divisive components we happened to get with PCA.

If you think about it, a mixture of these three factors can produce

basically the same patterns as the first three factors of the PCA, but

in a different way. Note that the PCA dimensions do not change as we

increase the number of dimensions–we do this once and pick off the first

few dimensions we care about. FA gives us the best model with a limited

number of factors (usually from a maximum likelihood perspective), and

it calculates a statistical test asking whether the model is sufficient,

at least if it can compute this. For f3, it cannot be calculated, and it

says the DF of the model is 0 and the fit is 0. For 1- and 2-factor

models, it tells us that 1-factor fails but 2-factor does not,

suggesting a 2-factor solution is sufficient.

f1 <- factanal(covmat = ability.cov, factors = 1)

f2 <- factanal(covmat = ability.cov, factors = 2)

f1

Call:

factanal(factors = 1, covmat = ability.cov)

Uniquenesses:

general picture blocks maze reading vocab

0.535 0.853 0.748 0.910 0.232 0.280

Loadings:

Factor1

general 0.682

picture 0.384

blocks 0.502

maze 0.300

reading 0.877

vocab 0.849

Factor1

SS loadings 2.443

Proportion Var 0.407

Test of the hypothesis that 1 factor is sufficient.

The chi square statistic is 75.18 on 9 degrees of freedom.

The p-value is 1.46e-12

Call:

factanal(factors = 2, covmat = ability.cov)

Uniquenesses:

general picture blocks maze reading vocab

0.455 0.589 0.218 0.769 0.052 0.334

Loadings:

Factor1 Factor2

general 0.499 0.543

picture 0.156 0.622

blocks 0.206 0.860

maze 0.109 0.468

reading 0.956 0.182

vocab 0.785 0.225

Factor1 Factor2

SS loadings 1.858 1.724

Proportion Var 0.310 0.287

Cumulative Var 0.310 0.597

Test of the hypothesis that 2 factors are sufficient.

The chi square statistic is 6.11 on 4 degrees of freedom.

The p-value is 0.191 Each variable is given a ‘uniqueness’ score, which is the error variance of that term–the unique variance not accounted for by the model. This can help identify whether there are measures that should be removed, because they are simply multiple measures of the same thing. Also, the factors show sum-of-squares (variance), proportion and cumulative, to give a basic effect size for each factor. Because the factors try to maximize variance, we see less of a fall-off in explained variance across factors, and the method balances variance more equally across factors. However, as we increase the number of factors, you can see the total additional variance accounted for per dimension tends to gets smaller. In this case, f1 accounted for 41%, f2 accounted for 50%, and f3 accounted for 67%.

Now that we see some of the similarities and differences, let’s examine the different arguments to factor analysis.

Input data

factanal can use a formula with the raw data, or a covariance or correlation matrix. When given data, it will form the covariance matrix. When given a formula, you specify nothing to the left of the ~, but any variable you care about to the right. If no formula is given, it will use all the variables.

Notice that each of the following produces exactly the same results:

A <- rnorm(100)

B <- rnorm(100)

C <- A + rnorm(100) * 5

D <- B + rnorm(100) * 5

E <- A - B + rnorm(100) * 4

F <- C + D + rnorm(100) * 5

data <- data.frame(A, B, C, D, E, F)

factanal(data, factors = 3)

Call:

factanal(x = data, factors = 3)

Uniquenesses:

A B C D E F

0.937 0.791 0.453 0.005 0.005 0.005

Loadings:

Factor1 Factor2 Factor3

A 0.201 0.135

B 0.438 -0.128

C 0.733

D 0.273 0.946 0.158

E 0.101 -0.121 0.985

F 0.939 0.322

Factor1 Factor2 Factor3

SS loadings 1.545 1.219 1.039

Proportion Var 0.258 0.203 0.173

Cumulative Var 0.258 0.461 0.634

The degrees of freedom for the model is 0 and the fit was 0.0028

Call:

factanal(x = ~A + B + C + D + E + F, factors = 3, data = data)

Uniquenesses:

A B C D E F

0.937 0.791 0.453 0.005 0.005 0.005

Loadings:

Factor1 Factor2 Factor3

A 0.201 0.135

B 0.438 -0.128

C 0.733

D 0.273 0.946 0.158

E 0.101 -0.121 0.985

F 0.939 0.322

Factor1 Factor2 Factor3

SS loadings 1.545 1.219 1.039

Proportion Var 0.258 0.203 0.173

Cumulative Var 0.258 0.461 0.634

The degrees of freedom for the model is 0 and the fit was 0.0028

Call:

factanal(factors = 3, covmat = cov(data))

Uniquenesses:

A B C D E F

0.937 0.791 0.453 0.005 0.005 0.005

Loadings:

Factor1 Factor2 Factor3

A 0.201 0.135

B 0.438 -0.128

C 0.733

D 0.273 0.946 0.158

E 0.101 -0.121 0.985

F 0.939 0.322

Factor1 Factor2 Factor3

SS loadings 1.545 1.219 1.039

Proportion Var 0.258 0.203 0.173

Cumulative Var 0.258 0.461 0.634

The degrees of freedom for the model is 0 and the fit was 0.0028

Call:

factanal(factors = 3, covmat = cor(data))

Uniquenesses:

A B C D E F

0.937 0.791 0.453 0.005 0.005 0.005

Loadings:

Factor1 Factor2 Factor3

A 0.201 0.135

B 0.438 -0.128

C 0.733

D 0.273 0.946 0.158

E 0.101 -0.121 0.985

F 0.939 0.322

Factor1 Factor2 Factor3

SS loadings 1.545 1.219 1.039

Proportion Var 0.258 0.203 0.173

Cumulative Var 0.258 0.461 0.634

The degrees of freedom for the model is 0 and the fit was 0.0028 The psych library offers the fa() function

which has much more detailed output and other options. This function has

a lot of capabilities, but if we specify the varimax rotation, we get

nearly the same results:

Factor Analysis using method = minres

Call: psych::fa(r = (data), nfactors = 3, rotate = "varimax")

Standardized loadings (pattern matrix) based upon correlation matrix

MR1 MR3 MR2 h2 u2 com

A 0.20 0.08 0.13 0.064 0.9356 2.0

B -0.01 0.43 -0.13 0.202 0.7975 1.2

C 0.75 -0.10 0.00 0.572 0.4278 1.0

D 0.27 0.95 0.15 0.997 0.0033 1.2

E 0.11 -0.12 0.99 0.996 0.0038 1.1

F 0.92 0.33 0.09 0.960 0.0405 1.3

MR1 MR3 MR2

SS loadings 1.53 1.22 1.04

Proportion Var 0.26 0.20 0.17

Cumulative Var 0.26 0.46 0.63

Proportion Explained 0.40 0.32 0.27

Cumulative Proportion 0.40 0.73 1.00

Mean item complexity = 1.3

Test of the hypothesis that 3 factors are sufficient.

The degrees of freedom for the null model are 15 and the objective function was 1.51 with Chi Square of 144.89

The degrees of freedom for the model are 0 and the objective function was 0

The root mean square of the residuals (RMSR) is 0.01

The df corrected root mean square of the residuals is NA

The harmonic number of observations is 100 with the empirical chi square 0.24 with prob < NA

The total number of observations was 100 with Likelihood Chi Square = 0.36 with prob < NA

Tucker Lewis Index of factoring reliability = -Inf

Fit based upon off diagonal values = 1

Measures of factor score adequacy

MR1 MR3 MR2

Correlation of (regression) scores with factors 0.98 1.00 1.00

Multiple R square of scores with factors 0.95 1.00 0.99

Minimum correlation of possible factor scores 0.90 0.99 0.99Because these different functions all end up calculating correlations, this means that missing data (with NA values) can be troublesome. To deal with it, you can specify an na.action, including imputing a prediction about the missing values or ignoring them. Alternately, you can handle this when you make the covariance or correlation matrix.

Factor Analysis using method = minres

Call: fa(r = data, nfactors = 3)

Standardized loadings (pattern matrix) based upon correlation matrix

MR1 MR3 MR2 h2 u2 com

A 0.18 0.07 0.11 0.064 0.9356 2.0

B -0.09 0.44 -0.19 0.202 0.7975 1.4

C 0.81 -0.22 -0.01 0.572 0.4278 1.1

D 0.04 0.98 0.02 0.997 0.0033 1.0

E 0.00 0.00 1.00 0.996 0.0038 1.0

F 0.88 0.21 0.02 0.960 0.0405 1.1

MR1 MR3 MR2

SS loadings 1.48 1.26 1.05

Proportion Var 0.25 0.21 0.17

Cumulative Var 0.25 0.46 0.63

Proportion Explained 0.39 0.33 0.28

Cumulative Proportion 0.39 0.72 1.00

With factor correlations of

MR1 MR3 MR2

MR1 1.00 0.37 0.14

MR3 0.37 1.00 0.05

MR2 0.14 0.05 1.00

Mean item complexity = 1.3

Test of the hypothesis that 3 factors are sufficient.

df null model = 15 with the objective function = 1.51 with Chi Square = 144.89

df of the model are 0 and the objective function was 0

The root mean square of the residuals (RMSR) is 0.01

The df corrected root mean square of the residuals is NA

The harmonic n.obs is 100 with the empirical chi square 0.24 with prob < NA

The total n.obs was 100 with Likelihood Chi Square = 0.36 with prob < NA

Tucker Lewis Index of factoring reliability = -Inf

Fit based upon off diagonal values = 1

Measures of factor score adequacy

MR1 MR3 MR2

Correlation of (regression) scores with factors 0.98 1.00 1.00

Multiple R square of scores with factors 0.96 1.00 1.00

Minimum correlation of possible factor scores 0.91 0.99 0.99## try missing data:

data$A[30] <- NA

# factanal(data,factors=3) ## this does not work

# factanal(data,factors=3,na.action=na.omit) ## also does not work

factanal(~A + B + C + D + E + F, data = data, factors = 3, na.action = na.omit) ##this does

Call:

factanal(x = ~A + B + C + D + E + F, factors = 3, data = data, na.action = na.omit)

Uniquenesses:

A B C D E F

0.936 0.801 0.453 0.005 0.005 0.005

Loadings:

Factor1 Factor2 Factor3

A 0.198 0.146

B 0.431 -0.111

C 0.733

D 0.269 0.946 0.166

E -0.110 0.987

F 0.938 0.322 0.107

Factor1 Factor2 Factor3

SS loadings 1.537 1.210 1.047

Proportion Var 0.256 0.202 0.174

Cumulative Var 0.256 0.458 0.632

The degrees of freedom for the model is 0 and the fit was 0.0022 Factor Analysis using method = minres

Call: fa(r = data, nfactors = 3)

Standardized loadings (pattern matrix) based upon correlation matrix

MR1 MR3 MR2 h2 u2 com

A 0.18 0.06 0.12 0.066 0.9341 2.1

B -0.09 0.44 -0.19 0.202 0.7976 1.4

C 0.81 -0.22 -0.01 0.567 0.4328 1.1

D 0.04 0.98 0.02 0.997 0.0032 1.0

E 0.00 0.00 1.00 0.996 0.0038 1.0

F 0.88 0.21 0.02 0.965 0.0347 1.1

MR1 MR3 MR2

SS loadings 1.49 1.26 1.05

Proportion Var 0.25 0.21 0.18

Cumulative Var 0.25 0.46 0.63

Proportion Explained 0.39 0.33 0.28

Cumulative Proportion 0.39 0.72 1.00

With factor correlations of

MR1 MR3 MR2

MR1 1.00 0.37 0.14

MR3 0.37 1.00 0.05

MR2 0.14 0.05 1.00

Mean item complexity = 1.3

Test of the hypothesis that 3 factors are sufficient.

df null model = 15 with the objective function = 1.51 with Chi Square = 145.07

df of the model are 0 and the objective function was 0

The root mean square of the residuals (RMSR) is 0.01

The df corrected root mean square of the residuals is NA

The harmonic n.obs is 100 with the empirical chi square 0.2 with prob < NA

The total n.obs was 100 with Likelihood Chi Square = 0.32 with prob < NA

Tucker Lewis Index of factoring reliability = -Inf

Fit based upon off diagonal values = 1

Measures of factor score adequacy

MR1 MR3 MR2

Correlation of (regression) scores with factors 0.98 1.00 1.00

Multiple R square of scores with factors 0.96 1.00 1.00

Minimum correlation of possible factor scores 0.92 0.99 0.99Optimization method.

Factor analysis can be thought of as a model of the correlation matrix using a fixed number of hidden or latent predictors to describe the data. How this works is that the factor analysis method essentially tries to do PCA using an iterative approximation, with the restriction that you are forced to use a fixed number of factors. After starting at some solution, it iteratively refines this to best describe the data better and maximize goodness of fit of the model or minimize error in order to best describe the covariance data. However, it is not always exactly clear what ‘best describe the data’ means. Some traditional methods are ‘minres’, maximum likelihood, and principal axes, but other methods are available for special cases, depending on the software. In general, choice of optimization method probably depends more on requirements such as size, missing values, availability in the software you are using, etc. The results might not differ much, one probably won’t be universally better for all data sets, and results will be more impacted by other things such as the rotation. The literature suggests that the particular optimization methods differ across software packages, are not well documented, and typically produce similar results. Most sources appear to recommend using ML as a default if the matrix is well-behaved, and if it is not (i.e., the model does not converge) to try another method. The ML (maximum likelihood) factor analysis attempts to find a solution that is most likely to have produced the correlation matrix. Some methods will warn about ‘Heywood cases’ which could signal that another optimization method could be tried.

The factanal function in R uses ML and has a number of

options for controlling the estimation; the fa function in in the psych

offers more alternatives to ML, but its ML implementation has fewer

options. We will also use the psych::fa function because of better

output, but you might try an alternate implementation if you run into

trouble.

Rotations

Once a solution has been produced, we will have a small fixed number of components/factors that hopefully do a good job a redescribing the complete correlation matrix. But we have a potential problem of non-identifiability. These base factors will be orthogonal just as in PCA, which means that any point (i.e, a response pattern across questions) can be described as a combination of factors. But there are rotations of these axes that produce equally good fits. Thus, once the analysis is done, one usually chooses one of a number of rotations for looking at the data. Some common ones are available within the GPArotation library in R, and can be applied either as a function of fa, or afterward.

It might seem non-intuitive that the rotation is not a part of the optimizization. But unlike PCA which has a very well-defined way of assigning dimensions (each dimension maximizes variance in that direction, subject to being orthogonal to all others), factor analysis finds its solution to minimize residual variance/maximize goodness-of-fit. Consequently, it is more like MDS, in that a particular dimension that it picks may not be the best or most meaningful dimension to look at. A specific rotation may help, and often leads to more interpretable factors, because they are designed to hang together better and account for distinct variance. These rotations are available within several packages, including GPArotation, which is used by psych::fa.

varimax (variance maximizing rotation). This maximizes the variance of the factors. Because variance involves squared deviation, it is best to try to put all the variance of any question into a single factor, rather than spreading it out. So overall, factors should favor all-or-none membership of items. Thus it tries to align factors with measures that vary. This is the most popular orthogonal rotation method used frequently by default, and aims to find a simple model where questions are related to unique factors. Within psych::fa, it is no longer the default; as that package uses a non-orthogonal rotation.

quartimax. This maximizes the variance in each item (rather than each factor). Again, this aims for a simple model. To maximize the variance of each item, it should also be placed in a single factor, so it is described as minimizing the number of factors an item appears in.

equamax uses a weighted sum of varimax and quartimax.

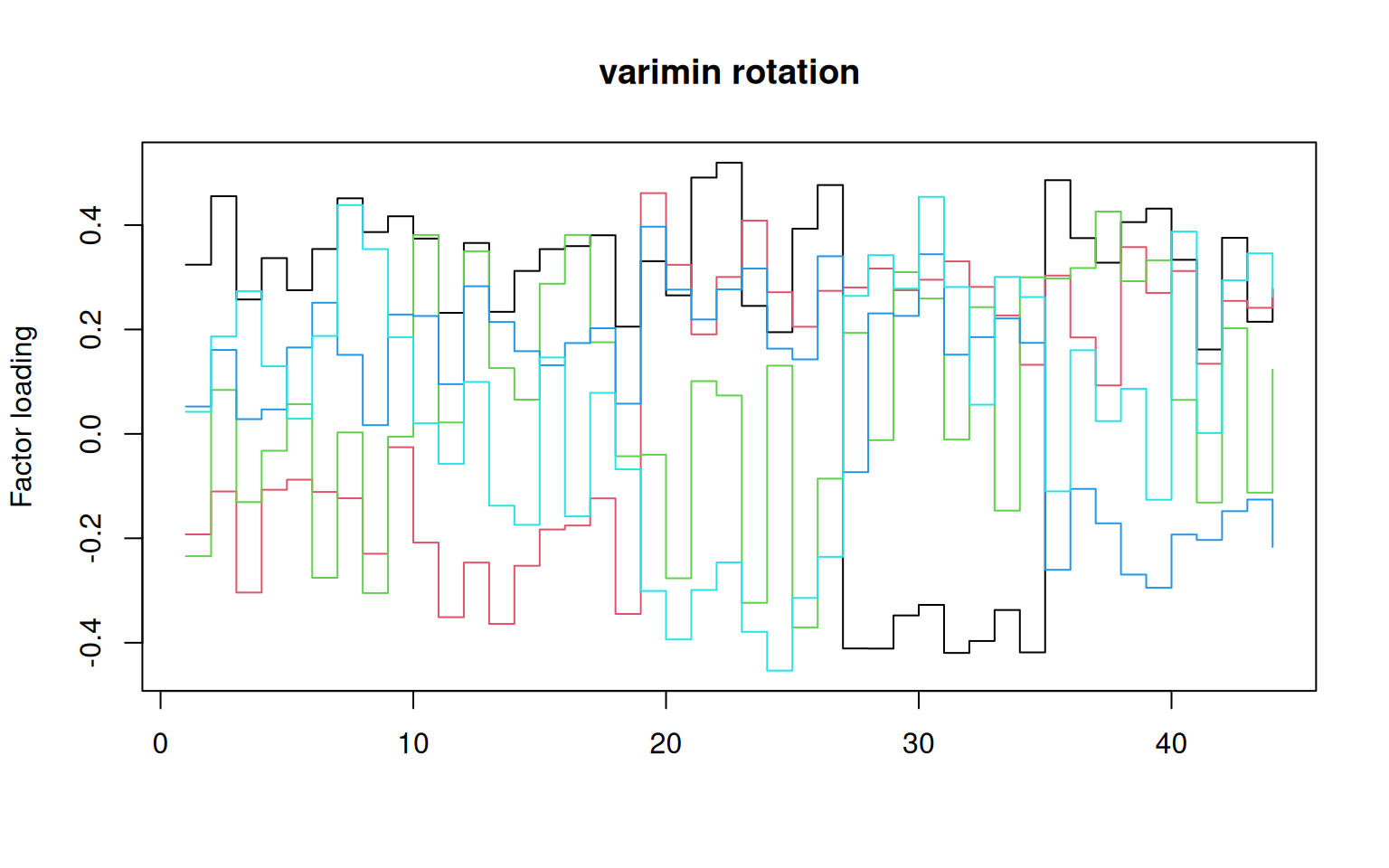

varimin a does the opposite of what varimax does. It tries to minimize the variance of each item, so that each item is spread out across factors. This is useful when you have a lot of items that are not well described by a single factor.

geominT is a compromise between varimax and quartimax, and is often used when you have a lot of items that are not well described by a single factor.

bifactor is a special rotation that is used when you have a general factor and a number of specific factors. It is used to separate the general and specific factors. This is a special case of the oblique rotations, and is used when you have a general factor that is correlated with all the other factors.

A list of available orthogonal rotations includes: “none”, “varimax”, “quartimax”, “bentlerT”, “equamax”, “varimin”, “geominT” and “bifactor”

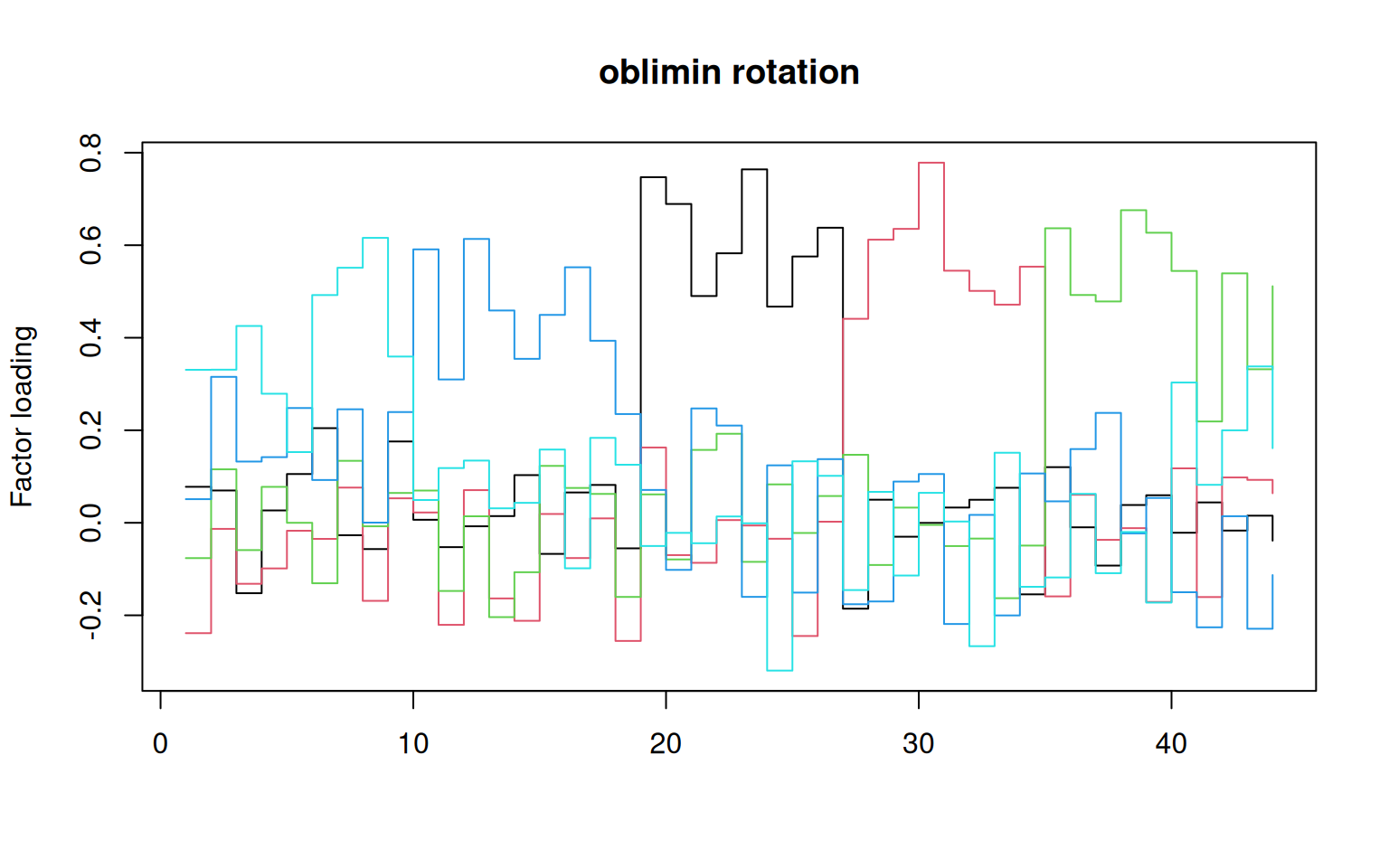

The above are all ‘orthogonal’ rotations–they require the factors to be independent and at right angles to one another. But it may be better if we allow the factors to be somewhat correlated if they are able to simplify the model more. These are not exactly rotations, because they are also essentially warping the dimensions of the space. They are more properly called ‘oblique transformations’.

The oblique transformations are harder to easily describe. They use differing criteria to try to create simple and interpretable models. For oblique transformations, the factors will be correlated with one another. However, the correlation cannot be too large, because then it would be better to combine those factors into a single factor.

Some options include the following. These are not well documented, and so it is usually preferable to use one that is well understood than to use one you cannot justify, but sometimes an exotic rotation will show a view of your data you did not see anywhere else. Many of the orthogonal rotations have oblique versions, where the orthogonal rotation ends with a T and the oblique ends with a Q.

- oblimin (default of the fa function).

- promax: an oblique transformation that has been described as having similar goals to varimax.

- simplimax: a simple structure oblique transformation that tries to maximize the variance of each item on a single factor.

- bentlerQ: a transformation that tries to maximize the variance of each item on a single factor, but also tries to minimize the number of factors each item appears in.

- geominQ: an oblique geomin.

- quartimin: a transformation that tries to minimize the variance of each item on a single factor.

- cluster: a transformation that tries to group items into clusters that are highly correlated with one another, but not with other clusters.

Example: Big Five data set

Let’s try reading in the big-five data set and performing a factor analysis with various different rotations. We will use the big five data, and both fa and factanal will take the entire data set directly, and not require you to compute a correlation matrix first.

Read in the big-five data set:

data <- read.csv("bigfive.csv")

dat.vals <- data[, -1] ##remove subject code

qtype <- c("E", "A", "C", "N", "O", "E", "A", "C", "N", "O", "E", "A", "C", "N",

"O", "E", "A", "C", "N", "O", "E", "A", "C", "N", "O", "E", "A", "C", "N", "O",

"E", "A", "C", "N", "O", "E", "A", "C", "N", "O", "O", "A", "C", "O")

valence <- c(1, -1, 1, 1, 1, -1, 1, -1, -1, 1, 1, -1, 1, 1, 1, 1, 1, -1, 1, 1, -1,

1, -1, -1, 1, 1, -1, 1, 1, 1, -1, 1, 1, -1, -1, 1, -1, 1, 1, 1, -1, 1, -1, 1)

add <- c(6, 0, 0)[valence + 2]

tmp <- dat.vals

tmp[is.na(tmp)] <- 3.5

reversed <- t(t(tmp) * valence + add)

## reverse code questions:

bytype <- reversed[, order(qtype)]

key <- sort(qtype)

colnames(bytype) <- paste(key, 1:44, sep = "")#Factor analysis functions

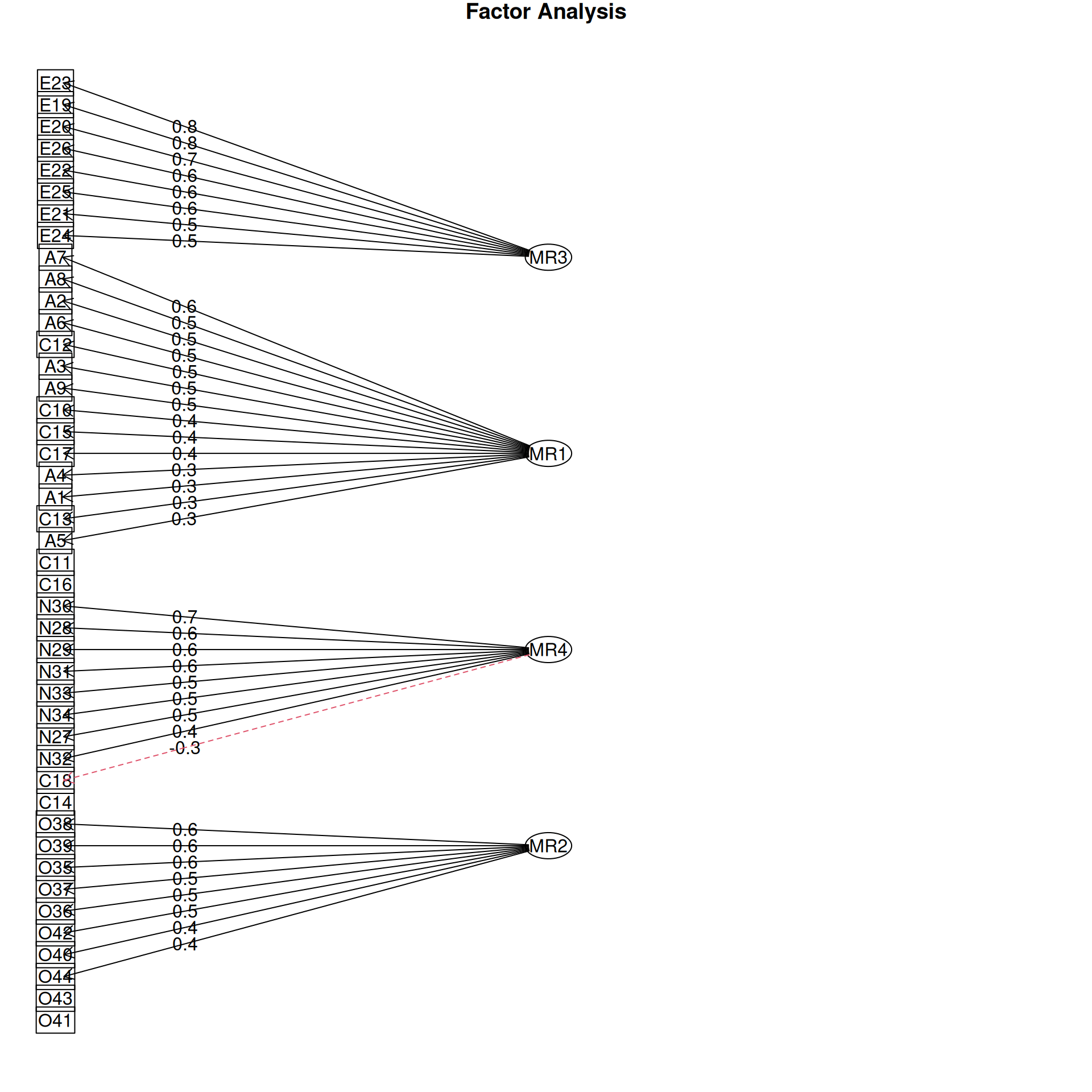

First, let’s confirm that the different fa methods can produce similar results:

Call:

factanal(x = bytype, factors = 3)

Uniquenesses:

A1 A2 A3 A4 A5 A6 A7 A8 A9 C10 C11 C12 C13

0.859 0.772 0.844 0.883 0.912 0.896 0.748 0.840 0.829 0.766 0.833 0.768 0.836

C14 C15 C16 C17 C18 E19 E20 E21 E22 E23 E24 E25 E26

0.820 0.770 0.797 0.815 0.835 0.450 0.521 0.589 0.502 0.447 0.734 0.599 0.543

N27 N28 N29 N30 N31 N32 N33 N34 O35 O36 O37 O38 O39

0.633 0.661 0.663 0.614 0.656 0.727 0.799 0.707 0.674 0.691 0.753 0.667 0.728

O40 O41 O42 O43 O44

0.738 0.984 0.685 0.912 0.797

Loadings:

Factor1 Factor2 Factor3

A1 0.367

A2 0.276 0.386

A3 0.328 0.125 -0.181

A4 0.250 0.233

A5 0.199 0.200

A6 0.278 0.105 0.125

A7 0.231 0.439

A8 0.354 0.160

A9 0.206 0.333 0.132

C10 0.277 0.397

C11 0.405

C12 0.278 0.393

C13 0.401

C14 0.398 0.121

C15 0.242 0.409

C16 0.299 0.318 0.111

C17 0.250 0.343

C18 0.403

E19 0.156 0.721

E20 0.682

E21 0.205 0.287 0.535

E22 0.132 0.335 0.607

E23 -0.111 0.735

E24 0.512

E25 0.236 0.585

[ reached getOption("max.print") -- omitted 19 rows ]

Factor1 Factor2 Factor3

SS loadings 4.219 3.854 3.631

Proportion Var 0.096 0.088 0.083

Cumulative Var 0.096 0.183 0.266

Test of the hypothesis that 3 factors are sufficient.

The chi square statistic is 5675.51 on 817 degrees of freedom.

The p-value is 0 Factor Analysis using method = minres

Call: fa(r = bytype, nfactors = 3, rotate = "varimax")

Standardized loadings (pattern matrix) based upon correlation matrix

MR1 MR2 MR3 h2 u2 com

A1 0.39 0.03 0.04 0.156 0.84 1.0

A2 0.33 0.38 0.02 0.250 0.75 2.0

A3 0.37 0.12 -0.22 0.197 0.80 1.9

A4 0.27 0.22 0.01 0.123 0.88 1.9

A5 0.23 0.18 0.07 0.091 0.91 2.2

A6 0.33 0.11 0.07 0.123 0.88 1.3

A7 0.29 0.44 -0.12 0.293 0.71 1.9

A8 0.40 0.16 -0.14 0.201 0.80 1.6

A9 0.25 0.33 0.10 0.178 0.82 2.1

C10 0.32 0.37 0.01 0.244 0.76 2.0

C11 0.44 0.00 -0.06 0.198 0.80 1.0

C12 0.34 0.37 -0.05 0.255 0.75 2.0

[ reached 'max' / getOption("max.print") -- omitted 32 rows ]

MR1 MR2 MR3

SS loadings 4.33 3.75 3.66

Proportion Var 0.10 0.09 0.08

Cumulative Var 0.10 0.18 0.27

Proportion Explained 0.37 0.32 0.31

Cumulative Proportion 0.37 0.69 1.00

Mean item complexity = 1.5

Test of the hypothesis that 3 factors are sufficient.

df null model = 946 with the objective function = 14.28 with Chi Square = 14284.11

df of the model are 817 and the objective function was 5.72

The root mean square of the residuals (RMSR) is 0.07

The df corrected root mean square of the residuals is 0.08

The harmonic n.obs is 1017 with the empirical chi square 9890.49 with prob < 0

The total n.obs was 1017 with Likelihood Chi Square = 5714.55 with prob < 0

Tucker Lewis Index of factoring reliability = 0.574

RMSEA index = 0.077 and the 90 % confidence intervals are 0.075 0.079

BIC = 57.14

Fit based upon off diagonal values = 0.83

Measures of factor score adequacy

MR1 MR2 MR3

Correlation of (regression) scores with factors 0.92 0.91 0.92

Multiple R square of scores with factors 0.84 0.83 0.85

Minimum correlation of possible factor scores 0.68 0.66 0.70

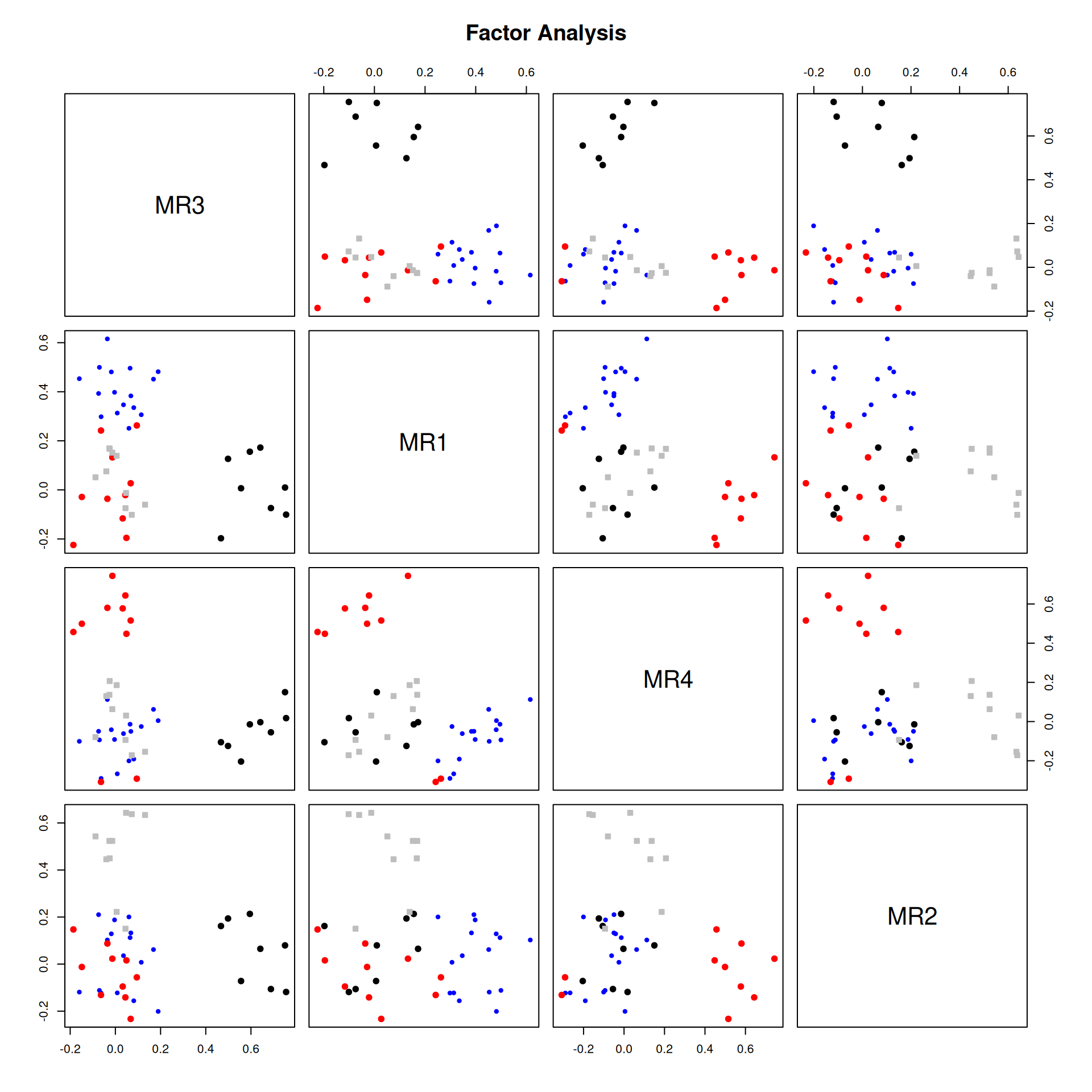

Notice that the two methods produce very similar results, but they display different information and show the factors differently. Let’s focus on the output of fa, which was done using the minres method; we could have also selected ml, wls, gls, or pa.

- It first shows a matrix that includes the three factors (MR2, MR3, and MR1), along with several other statistics. You can get this by doing loadings(model). This will display only the ‘important’ values–the values close to 0 will not be shown for easier examination.

- h2 is the communality score–sum of the squared factor loadings for each question. Somewhat like an \(R^2\) value for each item.

- u2 is the uniqueness score, 1-h2.

- com is complexity, an information score that is generally related to uniqueness.

Next, a number of statistics related to the model are shown. It then provides a chi-squared test of whether the model is sufficiently complex (or needs more factors), and other diagnostics of whether the model is acceptable. Because we guess there might be five, we will try five, using the ml optimization method

Optimization method

let’s look at different optimization methods, using the fm argument

Factor Analysis using method = ml

Call: psych::fa(r = bytype, nfactors = 5, rotate = "quartimax", fm = "ml")

Standardized loadings (pattern matrix) based upon correlation matrix

ML2 ML3 ML4 ML1 ML5 h2 u2 com

A1 0.10 -0.27 -0.05 0.08 0.33 0.20 0.80 2.3

A2 0.11 -0.07 0.17 0.34 0.35 0.29 0.71 2.7

A3 -0.13 -0.16 -0.04 0.15 0.43 0.25 0.75 1.8

A4 0.06 -0.13 0.11 0.17 0.29 0.14 0.86 2.5

A5 0.12 -0.06 0.05 0.26 0.17 0.11 0.89 2.5

A6 0.20 -0.09 -0.09 0.12 0.49 0.31 0.69 1.6

A7 0.00 0.02 0.18 0.28 0.57 0.43 0.57 1.7

A8 -0.04 -0.19 0.01 0.05 0.62 0.42 0.58 1.2

A9 0.19 -0.01 0.12 0.26 0.37 0.26 0.74 2.6

[ reached 'max' / getOption("max.print") -- omitted 35 rows ]

ML2 ML3 ML4 ML1 ML5

SS loadings 3.60 3.42 3.19 2.89 2.40

Proportion Var 0.08 0.08 0.07 0.07 0.05

Cumulative Var 0.08 0.16 0.23 0.30 0.35

Proportion Explained 0.23 0.22 0.21 0.19 0.16

Cumulative Proportion 0.23 0.45 0.66 0.84 1.00

Mean item complexity = 1.8

Test of the hypothesis that 5 factors are sufficient.

df null model = 946 with the objective function = 14.28 with Chi Square = 14284.11

df of the model are 736 and the objective function was 3.19

The root mean square of the residuals (RMSR) is 0.05

The df corrected root mean square of the residuals is 0.05

The harmonic n.obs is 1017 with the empirical chi square 4045.22 with prob < 0

The total n.obs was 1017 with Likelihood Chi Square = 3176.97 with prob < 3e-299

Tucker Lewis Index of factoring reliability = 0.764

RMSEA index = 0.057 and the 90 % confidence intervals are 0.055 0.059

BIC = -1919.54

Fit based upon off diagonal values = 0.93

Measures of factor score adequacy

ML2 ML3 ML4 ML1 ML5

Correlation of (regression) scores with factors 0.93 0.92 0.91 0.88 0.88

Multiple R square of scores with factors 0.86 0.84 0.82 0.78 0.77

Minimum correlation of possible factor scores 0.73 0.68 0.65 0.56 0.53Factor Analysis using method = gls

Call: psych::fa(r = bytype, nfactors = 5, rotate = "quartimax", fm = "gls")

Standardized loadings (pattern matrix) based upon correlation matrix

GLS3 GLS4 GLS2 GLS5 GLS1 h2 u2 com

A1 0.11 -0.27 -0.08 0.06 0.41 0.26 0.74 2.0

A2 0.11 -0.06 0.19 0.31 0.40 0.31 0.69 2.6

A3 -0.15 -0.16 -0.03 0.14 0.48 0.29 0.71 1.6

A4 0.07 -0.12 0.11 0.12 0.37 0.18 0.82 1.8

A5 0.15 -0.04 0.04 0.23 0.25 0.14 0.86 2.8

A6 0.20 -0.08 -0.09 0.11 0.54 0.35 0.65 1.5

A7 0.00 0.02 0.23 0.23 0.56 0.42 0.58 1.7

A8 -0.06 -0.20 0.02 0.05 0.59 0.40 0.60 1.3

A9 0.21 0.00 0.15 0.22 0.41 0.28 0.72 2.5

[ reached 'max' / getOption("max.print") -- omitted 35 rows ]

GLS3 GLS4 GLS2 GLS5 GLS1

SS loadings 3.66 3.44 3.31 2.98 2.57

Proportion Var 0.08 0.08 0.08 0.07 0.06

Cumulative Var 0.08 0.16 0.24 0.30 0.36

Proportion Explained 0.23 0.22 0.21 0.19 0.16

Cumulative Proportion 0.23 0.44 0.65 0.84 1.00

Mean item complexity = 1.7

Test of the hypothesis that 5 factors are sufficient.

df null model = 946 with the objective function = 14.28 with Chi Square = 14284.11

df of the model are 736 and the objective function was 3.24

The root mean square of the residuals (RMSR) is 0.05

The df corrected root mean square of the residuals is 0.05

The harmonic n.obs is 1017 with the empirical chi square 4075.95 with prob < 0

The total n.obs was 1017 with Likelihood Chi Square = 3227.68 with prob < 9.7e-308

Tucker Lewis Index of factoring reliability = 0.759

RMSEA index = 0.058 and the 90 % confidence intervals are 0.056 0.06

BIC = -1868.83

Fit based upon off diagonal values = 0.93

Measures of factor score adequacy

GLS3 GLS4 GLS2 GLS5 GLS1

Correlation of (regression) scores with factors 0.93 0.92 0.92 0.90 0.90

Multiple R square of scores with factors 0.87 0.85 0.85 0.82 0.81

Minimum correlation of possible factor scores 0.73 0.70 0.70 0.63 0.62If you look at the loadings, values, etc. the factor analysis solutions are numerically different but tend to be fairly similar.

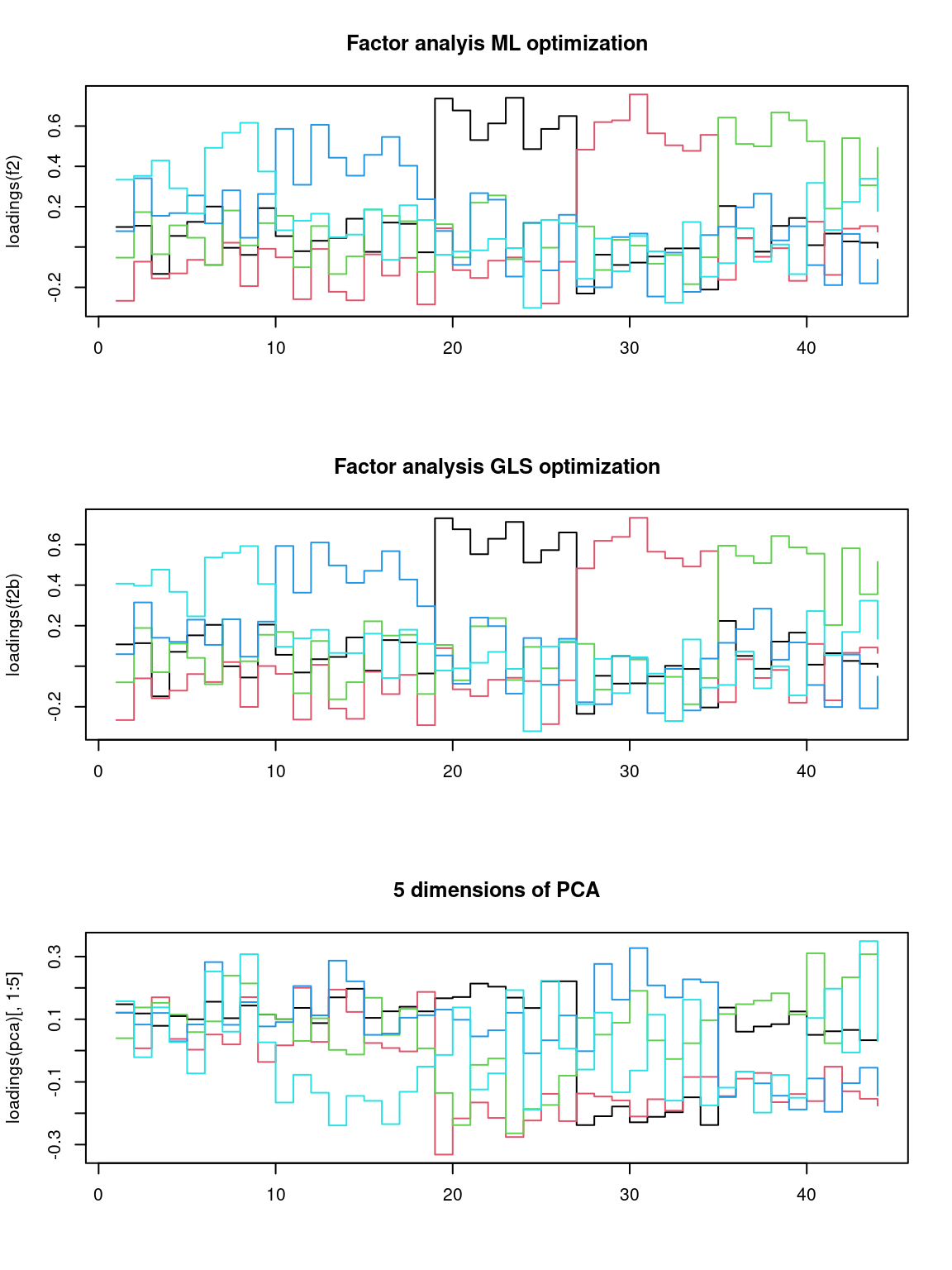

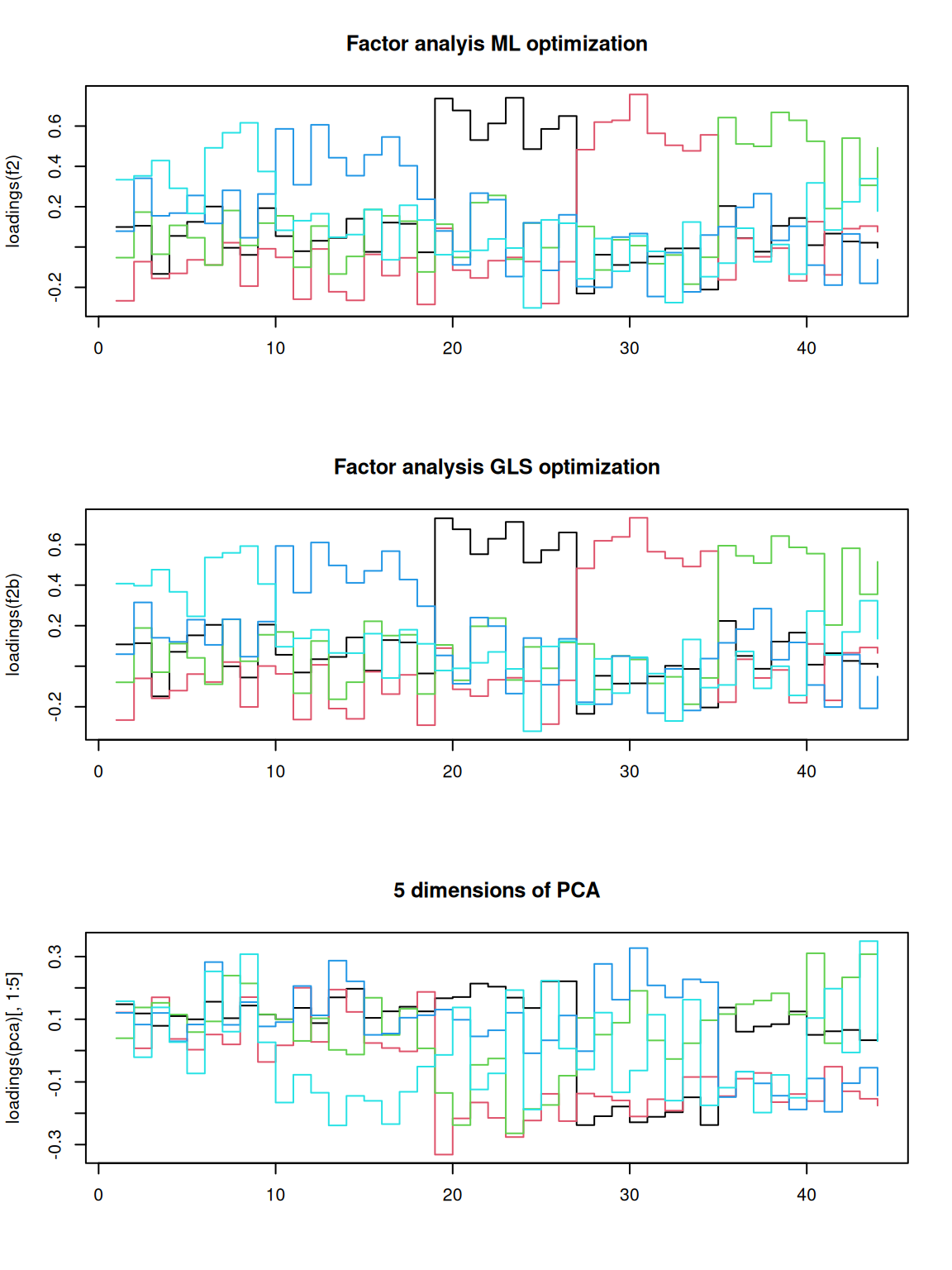

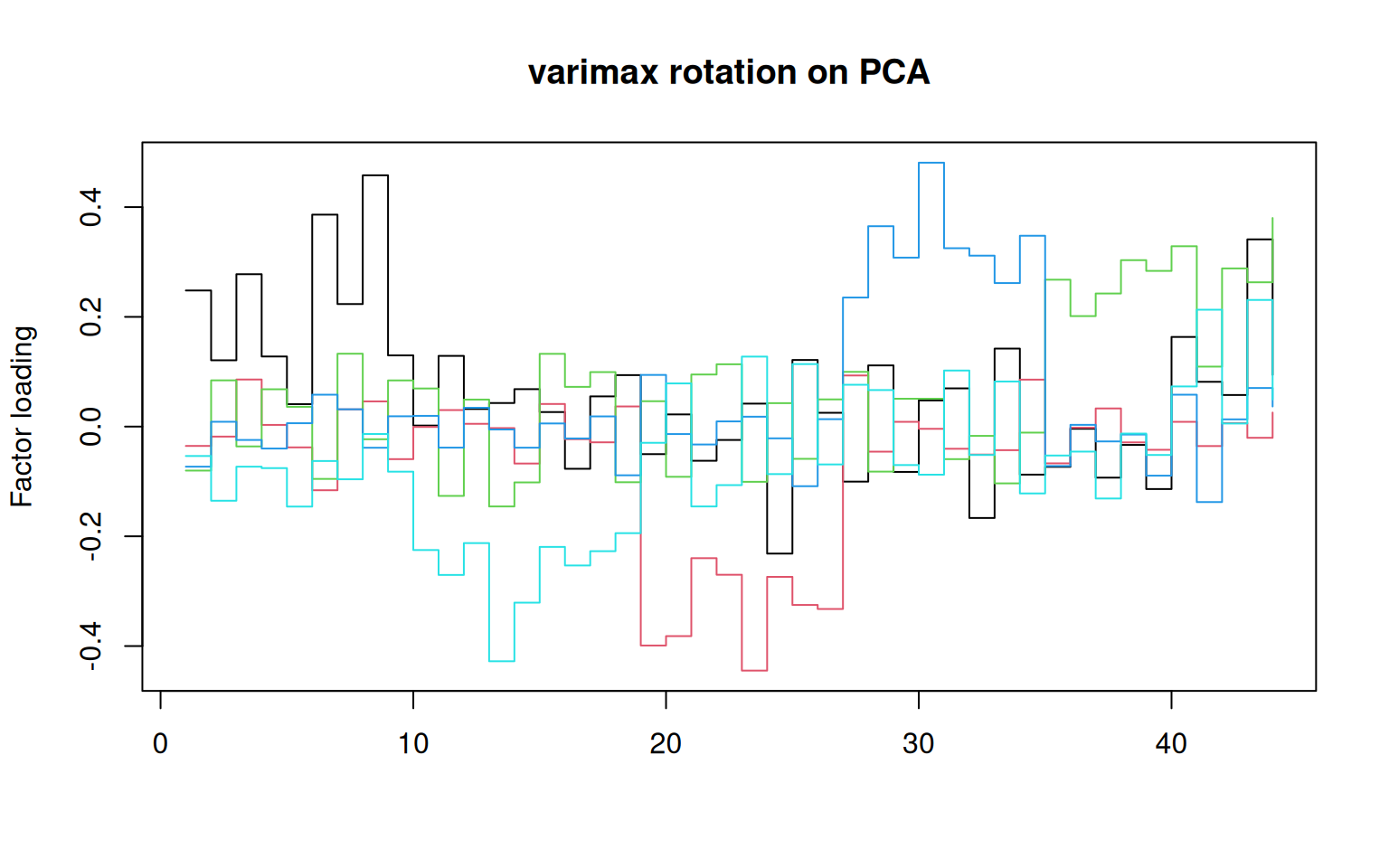

We can look at them specifically, especially in comparison to the PCA solution:

par(mfrow = c(3, 1))

matplot(loadings(f2), type = "s", lty = 1, main = "Factor analyis ML optimization")

matplot(loadings(f2b), type = "s", lty = 1, main = "Factor analysis GLS optimization")

matplot(loadings(pca)[, 1:5], main = "5 dimensions of PCA", type = "s", lty = 1) That does not look bad. If you compare to the factor loadings from the

PCA, these are much cleaner–the PCA is almost uninterpretable in

comparison. Notice that the two optimization methods produce results

that are essentially the same. It looks like each factor takes a turn

and maps roughly onto a different set of personality questions. This

structure comes from the quartimax rotation, not the optimization

method. But maybe other rotations would provide a stronger factor

structure. Although we applied rotations within the fa, we can also do

it afterward:

That does not look bad. If you compare to the factor loadings from the

PCA, these are much cleaner–the PCA is almost uninterpretable in

comparison. Notice that the two optimization methods produce results

that are essentially the same. It looks like each factor takes a turn

and maps roughly onto a different set of personality questions. This

structure comes from the quartimax rotation, not the optimization

method. But maybe other rotations would provide a stronger factor

structure. Although we applied rotations within the fa, we can also do

it afterward:

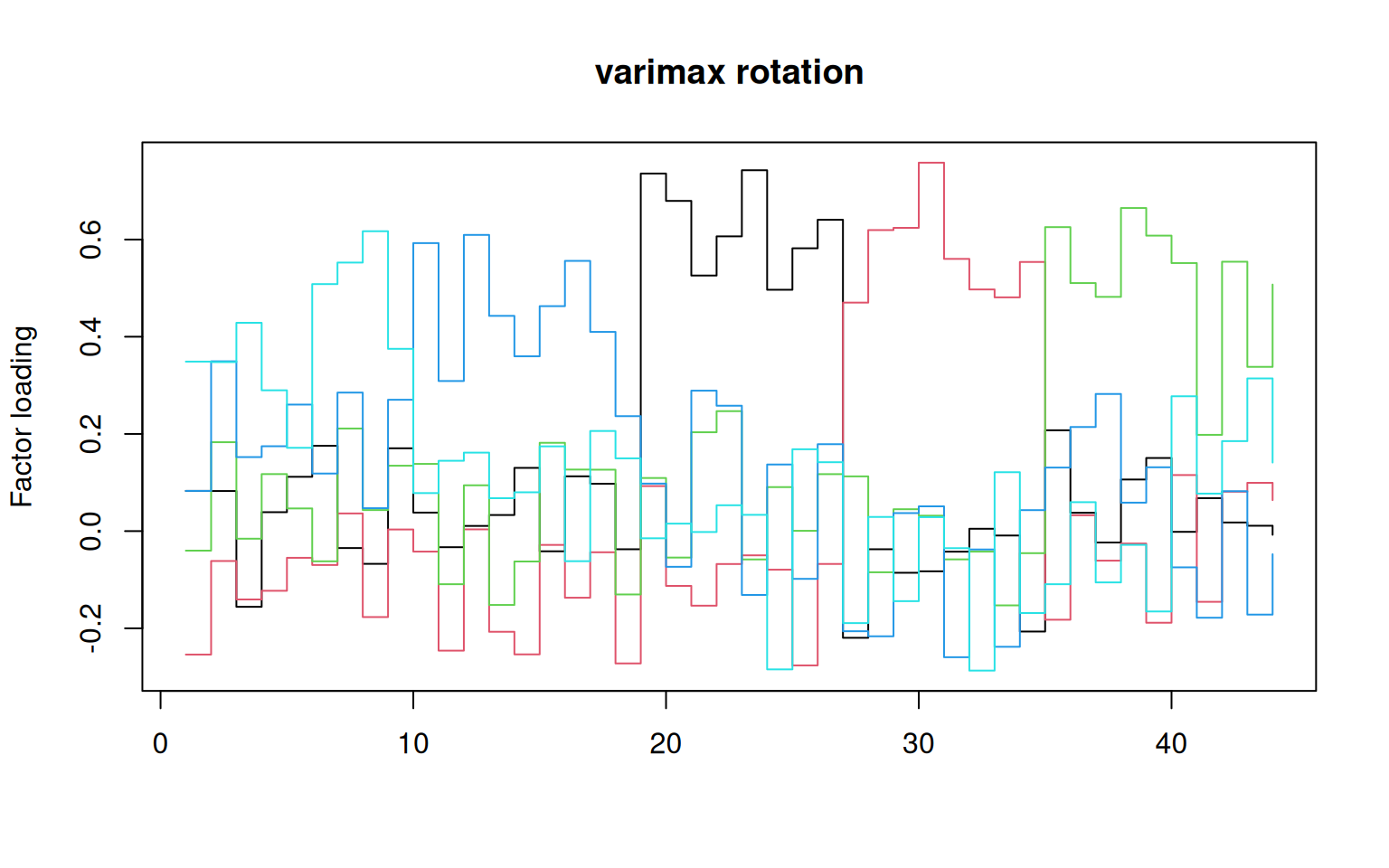

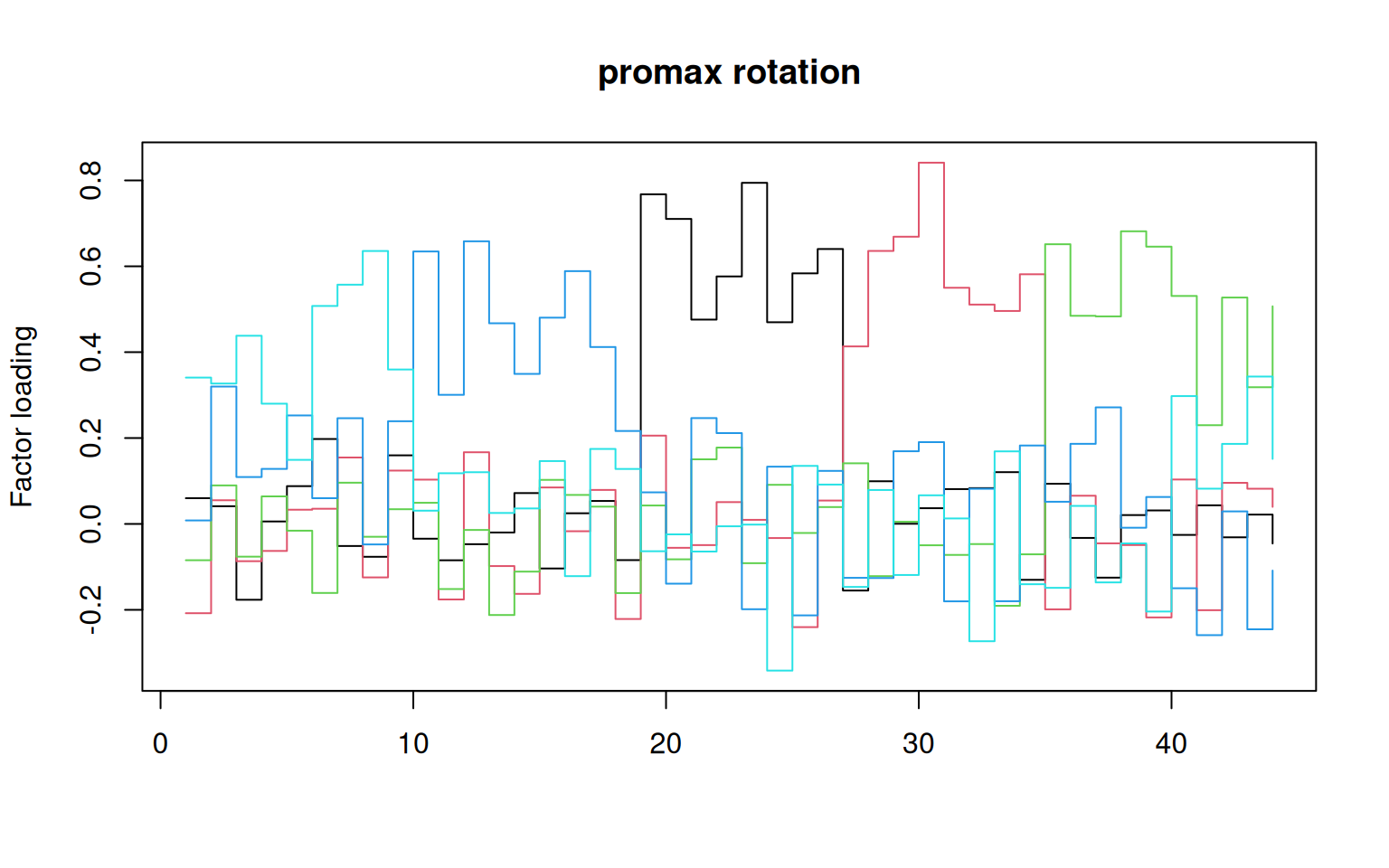

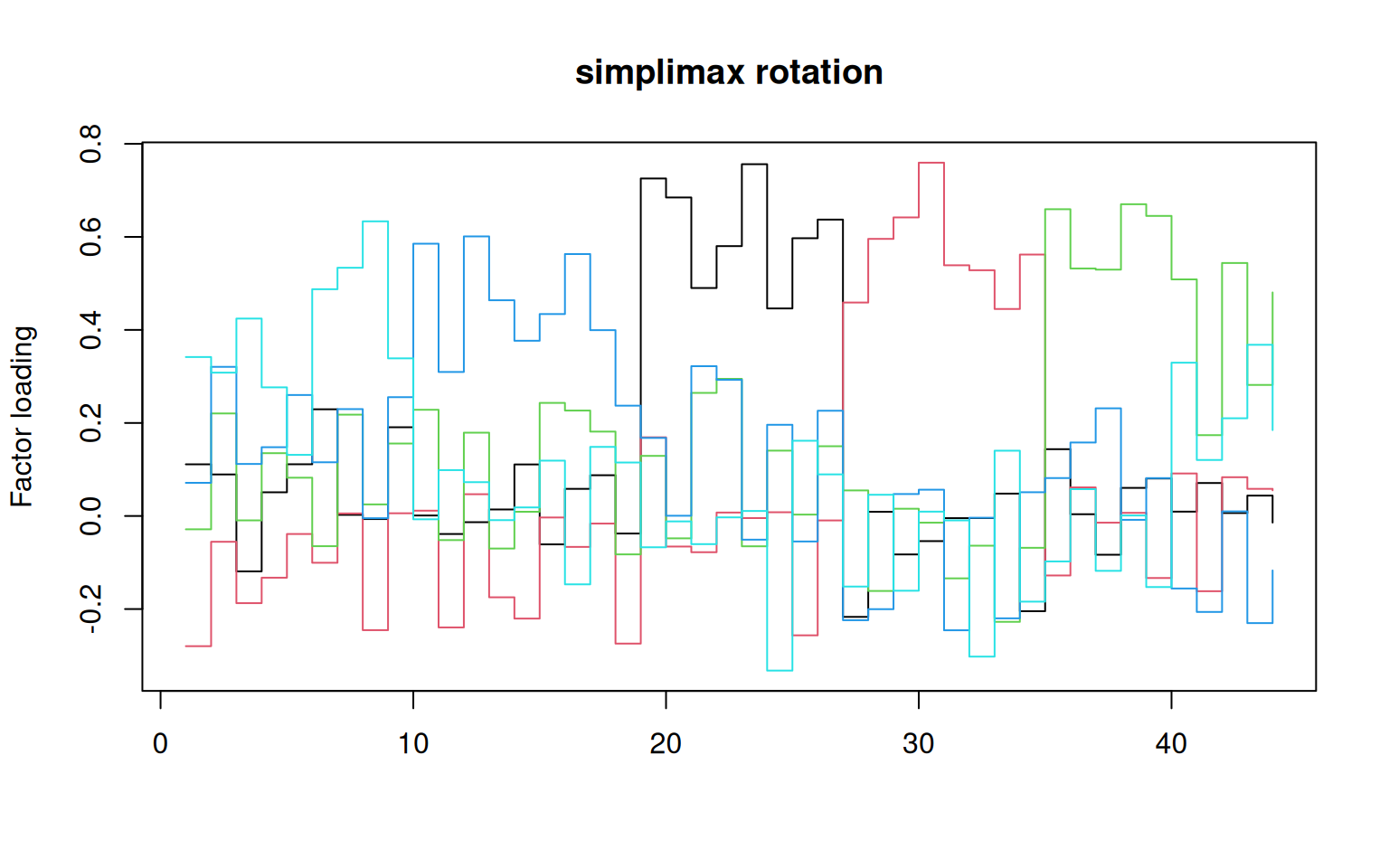

library(GPArotation) ##needed for rotations like oblimin

matplot(varimax(loadings(f2))$loadings, type = "s", lty = 1, main = "varimax rotation",

ylab = "Factor loading")

## fairly similar:

matplot(promax(loadings(f2))$loadings, type = "s", lty = 1, main = "promax rotation",

ylab = "Factor loading")

# matplot(oblimin(loadings(f2))$loadings,type='s',lty=1,main='oblimin

# rotation',ylab='Factor loading')

matplot(simplimax(loadings(f2))$loadings, type = "s", lty = 1, main = "simplimax rotation",

ylab = "Factor loading")

matplot(oblimin(loadings(f2))$loadings, type = "s", lty = 1, main = "oblimin rotation",

ylab = "Factor loading")

matplot(varimin(loadings(f2))$loadings, type = "s", lty = 1, main = "varimin rotation",

ylab = "Factor loading")

matplot(varimax(loadings(pca)[, 1:5])$loadings, type = "s", lty = 1, main = "varimax rotation on PCA",

ylab = "Factor loading")

Oblique rotations

If you use an oblique rotation, that means your factors are allowed to be correlated. Here is the full output of an oblique rotation (the oblimin):

Oblique rotation method Oblimin Quartimin converged.

Loadings:

ML2 ML3 ML4 ML1 ML5

A1 0.077792 -0.23858 -7.63e-02 0.051032 0.33072

A2 0.069772 -0.01312 1.16e-01 0.315380 0.33088

A3 -0.152205 -0.13186 -5.90e-02 0.132431 0.42540

A4 0.026625 -0.09872 7.76e-02 0.141818 0.27891

A5 0.105436 -0.01721 -2.08e-05 0.248122 0.15284

A6 0.204566 -0.03480 -1.31e-01 0.092521 0.49229

A7 -0.026877 0.07607 1.34e-01 0.245298 0.55135

A8 -0.056847 -0.16881 -7.57e-03 0.000358 0.61589

A9 0.175793 0.05282 6.45e-02 0.239280 0.35933

C10 0.006554 0.02231 6.97e-02 0.590989 0.04922

C11 -0.052645 -0.22064 -1.47e-01 0.309812 0.11829

C12 -0.007519 0.07060 1.41e-02 0.613554 0.13442

C13 0.014447 -0.16356 -2.04e-01 0.458906 0.03127

C14 0.102986 -0.21189 -1.07e-01 0.354427 0.04308

C15 -0.067266 0.01906 1.23e-01 0.449388 0.15831

[ reached getOption("max.print") -- omitted 29 rows ]

ML2 ML3 ML4 ML1 ML5

SS loadings 3.522 3.351 3.173 3.028 2.418

Proportion Var 0.080 0.076 0.072 0.069 0.055

Cumulative Var 0.080 0.156 0.228 0.297 0.352

Phi:

ML2 ML3 ML4 ML1 ML5

ML2 1.0000 -0.1931 0.1603 0.113 0.0184

ML3 -0.1931 1.0000 -0.0149 -0.179 -0.0729

ML4 0.1603 -0.0149 1.0000 0.230 0.0818

ML1 0.1135 -0.1794 0.2296 1.000 0.1240

ML5 0.0184 -0.0729 0.0818 0.124 1.0000Here, no factors are correlated more than around .2 (see the Phi matrix) which is a constraint in the oblique rotation. The oblique rotations/transformations will sacrifice orthogonality a little in order to maximize another property, usually something about the shared variance of the items that load highly on a factor.

Choosing the right number of factors and evaluating goodness of fit

Like all of the methods we have used, it is tough to know how many factors there are. One approach is to use pca to identify how many factors to use (looking at the scree plot and eigen decomposition). Then do a factor analysis to pick a model with that many dimensions. You can also use the goodness-of-fit statistics reported in the model. Many times, the challenge is that in order to get a model whose goodness-of-fit is large enough to satisfy the basic advice, you need to add more factors than are really interpretable.

Several statistics are available for evaluating goodness of fit, and these can be used to assess the number of factors as well. Detailed tutorials are available at http://davidakenny.net/cm/fit.htm .

Many of the statistics are output from the factor analysis directly, but it may be convenient to use the VSS on the correlation matrix.

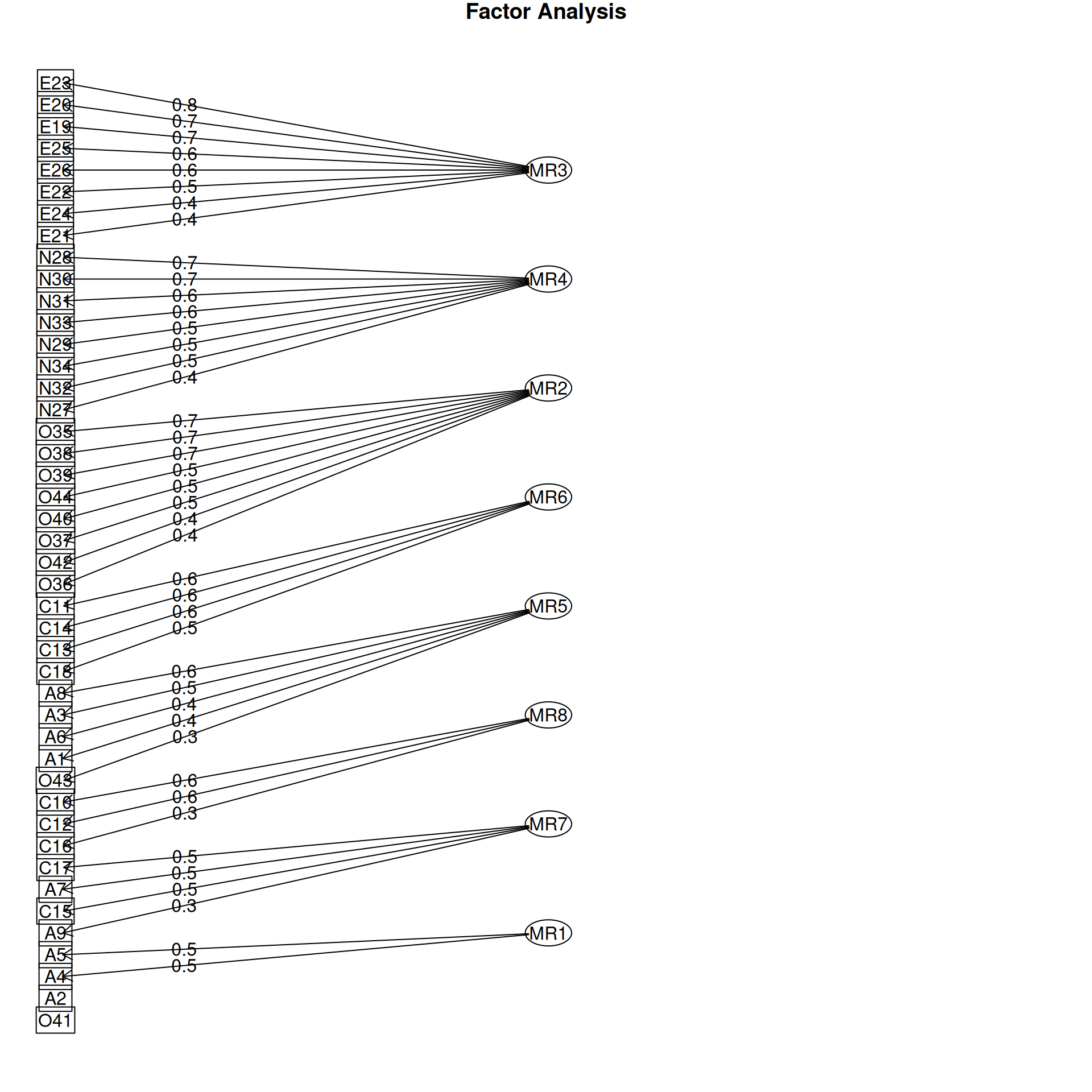

Factor analysis with Call: fa(r = bytype, nfactors = 5)

Test of the hypothesis that 5 factors are sufficient.

The degrees of freedom for the model is 736 and the objective function was 3.2

The number of observations was 1017 with Chi Square = 3193.66 with prob < 4.9e-302

The root mean square of the residuals (RMSA) is 0.05

The df corrected root mean square of the residuals is 0.05

Tucker Lewis Index of factoring reliability = 0.762

RMSEA index = 0.057 and the 10 % confidence intervals are 0.055 0.059

BIC = -1902.86

With factor correlations of

MR3 MR4 MR2 MR1 MR5

MR3 1.00 -0.19 0.16 0.13 0.02

MR4 -0.19 1.00 0.00 -0.20 -0.08

MR2 0.16 0.00 1.00 0.23 0.08

MR1 0.13 -0.20 0.23 1.00 0.14

MR5 0.02 -0.08 0.08 0.14 1.00

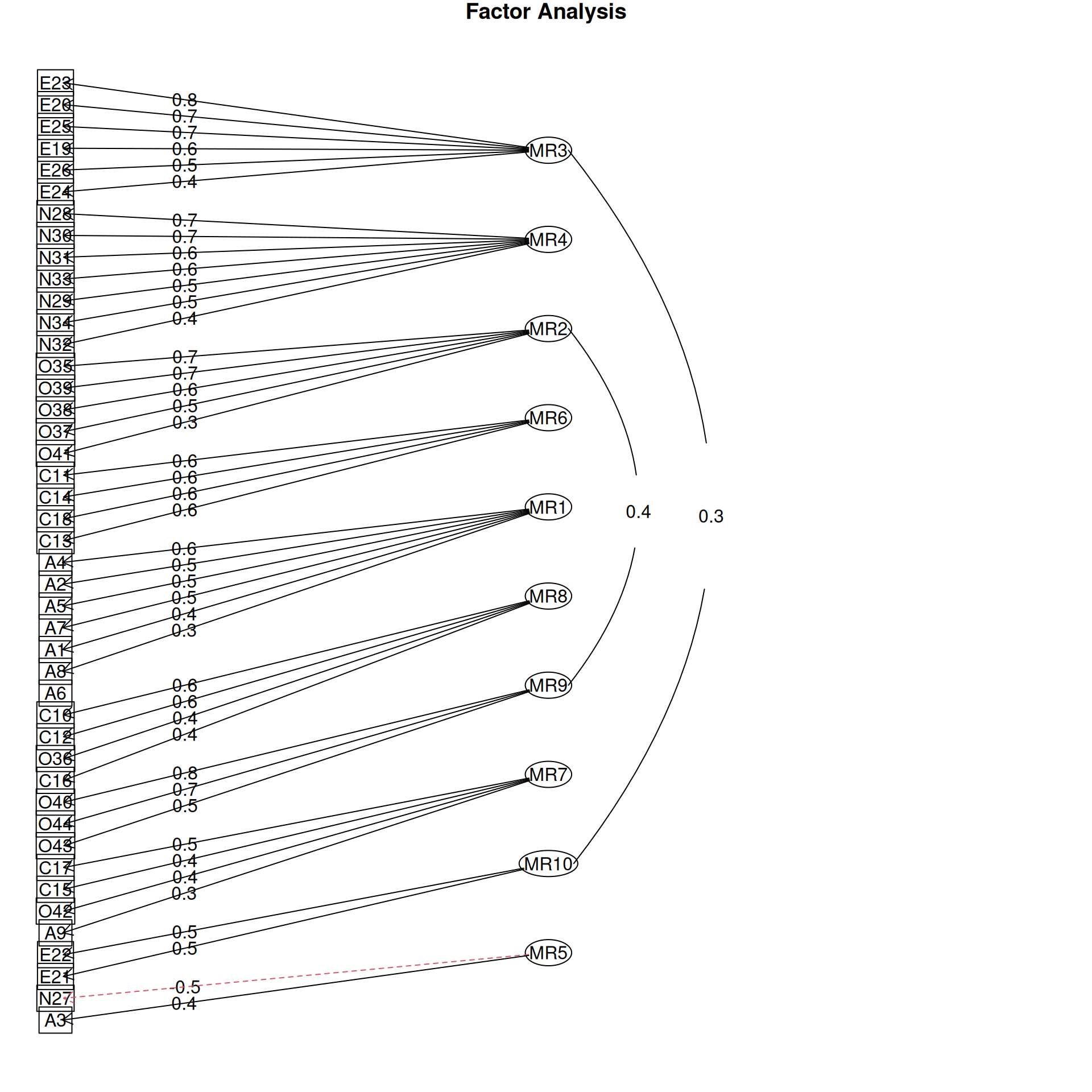

Factor analysis with Call: fa(r = bytype, nfactors = 8)

Test of the hypothesis that 8 factors are sufficient.

The degrees of freedom for the model is 622 and the objective function was 1.35

The number of observations was 1017 with Chi Square = 1342.04 with prob < 6.3e-55

The root mean square of the residuals (RMSA) is 0.02

The df corrected root mean square of the residuals is 0.03

Tucker Lewis Index of factoring reliability = 0.917

RMSEA index = 0.034 and the 10 % confidence intervals are 0.031 0.036

BIC = -2965.07

With factor correlations of

MR3 MR4 MR2 MR6 MR5 MR8 MR7 MR1

MR3 1.00 -0.18 0.16 0.12 -0.03 0.01 0.06 0.13

MR4 -0.18 1.00 -0.09 -0.30 -0.10 -0.09 -0.05 -0.12

MR2 0.16 -0.09 1.00 -0.04 0.01 0.20 0.20 0.11

MR6 0.12 -0.30 -0.04 1.00 0.10 0.18 0.03 0.02

MR5 -0.03 -0.10 0.01 0.10 1.00 -0.01 0.17 0.06

MR8 0.01 -0.09 0.20 0.18 -0.01 1.00 0.22 0.28

MR7 0.06 -0.05 0.20 0.03 0.17 0.22 1.00 0.08

MR1 0.13 -0.12 0.11 0.02 0.06 0.28 0.08 1.00Factor Analysis using method = minres

Call: fa(r = bytype, nfactors = 10)

Standardized loadings (pattern matrix) based upon correlation matrix

MR3 MR4 MR2 MR6 MR1 MR8 MR9 MR7 MR10 MR5 h2 u2 com

A1 0.04 -0.06 0.01 0.21 0.41 -0.10 0.02 -0.18 0.04 0.17 0.34 0.66 2.6

A2 0.08 -0.04 0.06 0.02 0.51 0.24 0.02 0.02 -0.07 -0.04 0.39 0.61 1.6

A3 -0.10 0.02 -0.03 0.13 0.28 0.17 0.04 -0.13 -0.12 0.37 0.37 0.63 3.5

A4 -0.06 -0.11 0.07 -0.07 0.61 -0.03 -0.03 -0.07 0.07 -0.02 0.40 0.60 1.2

A5 -0.04 -0.07 0.00 0.00 0.48 -0.01 -0.04 0.00 0.20 -0.14 0.30 0.70 1.6

[ reached 'max' / getOption("max.print") -- omitted 39 rows ]

MR3 MR4 MR2 MR6 MR1 MR8 MR9 MR7 MR10 MR5

SS loadings 2.95 2.83 2.43 2.11 2.02 1.83 1.66 1.49 1.39 1.19

Proportion Var 0.07 0.06 0.06 0.05 0.05 0.04 0.04 0.03 0.03 0.03

Cumulative Var 0.07 0.13 0.19 0.23 0.28 0.32 0.36 0.39 0.43 0.45

Proportion Explained 0.15 0.14 0.12 0.11 0.10 0.09 0.08 0.07 0.07 0.06

Cumulative Proportion 0.15 0.29 0.41 0.52 0.62 0.71 0.80 0.87 0.94 1.00

With factor correlations of

MR3 MR4 MR2 MR6 MR1 MR8 MR9 MR7 MR10 MR5

MR3 1.00 -0.15 0.18 0.10 0.03 -0.06 0.02 0.07 0.32 0.11

MR4 -0.15 1.00 -0.18 -0.27 -0.13 -0.04 0.11 -0.12 -0.10 -0.18

MR2 0.18 -0.18 1.00 0.00 0.08 0.21 0.38 0.09 0.17 -0.05

MR6 0.10 -0.27 0.00 1.00 0.11 0.15 -0.08 0.08 0.00 0.19

MR1 0.03 -0.13 0.08 0.11 1.00 0.21 0.18 0.16 0.17 0.29

MR8 -0.06 -0.04 0.21 0.15 0.21 1.00 0.10 0.21 0.22 -0.04

MR9 0.02 0.11 0.38 -0.08 0.18 0.10 1.00 0.24 -0.06 0.07

[ reached getOption("max.print") -- omitted 3 rows ]

Mean item complexity = 2.2

Test of the hypothesis that 10 factors are sufficient.

df null model = 946 with the objective function = 14.28 with Chi Square = 14284.11

df of the model are 551 and the objective function was 0.98

The root mean square of the residuals (RMSR) is 0.02

The df corrected root mean square of the residuals is 0.02

The harmonic n.obs is 1017 with the empirical chi square 602.99 with prob < 0.062

The total n.obs was 1017 with Likelihood Chi Square = 970.8 with prob < 1.3e-25

Tucker Lewis Index of factoring reliability = 0.946

RMSEA index = 0.027 and the 90 % confidence intervals are 0.025 0.03

BIC = -2844.66

Fit based upon off diagonal values = 0.99

Measures of factor score adequacy

MR3 MR4 MR2 MR6 MR1 MR8

Correlation of (regression) scores with factors 0.93 0.92 0.91 0.88 0.87 0.86

Multiple R square of scores with factors 0.86 0.84 0.82 0.77 0.76 0.75

Minimum correlation of possible factor scores 0.73 0.69 0.64 0.55 0.52 0.49

MR9 MR7 MR10 MR5

Correlation of (regression) scores with factors 0.88 0.84 0.85 0.81

Multiple R square of scores with factors 0.77 0.71 0.71 0.66

Minimum correlation of possible factor scores 0.55 0.42 0.43 0.31

Factor analysis with Call: fa(r = bytype, nfactors = 10)

Test of the hypothesis that 10 factors are sufficient.

The degrees of freedom for the model is 551 and the objective function was 0.98

The number of observations was 1017 with Chi Square = 970.8 with prob < 1.3e-25

The root mean square of the residuals (RMSA) is 0.02

The df corrected root mean square of the residuals is 0.02

Tucker Lewis Index of factoring reliability = 0.946

RMSEA index = 0.027 and the 10 % confidence intervals are 0.025 0.03

BIC = -2844.66

With factor correlations of

MR3 MR4 MR2 MR6 MR1 MR8 MR9 MR7 MR10 MR5

MR3 1.00 -0.15 0.18 0.10 0.03 -0.06 0.02 0.07 0.32 0.11

MR4 -0.15 1.00 -0.18 -0.27 -0.13 -0.04 0.11 -0.12 -0.10 -0.18

MR2 0.18 -0.18 1.00 0.00 0.08 0.21 0.38 0.09 0.17 -0.05

MR6 0.10 -0.27 0.00 1.00 0.11 0.15 -0.08 0.08 0.00 0.19

MR1 0.03 -0.13 0.08 0.11 1.00 0.21 0.18 0.16 0.17 0.29

MR8 -0.06 -0.04 0.21 0.15 0.21 1.00 0.10 0.21 0.22 -0.04

MR9 0.02 0.11 0.38 -0.08 0.18 0.10 1.00 0.24 -0.06 0.07

[ reached getOption("max.print") -- omitted 3 rows ][1] -1902.859 -2965.069 -2844.663Here, the 8-factor solution has the best BIC, the 4-factor solution has high RMSEA and low TLI, so it is probably not good.

Determining the number of factors

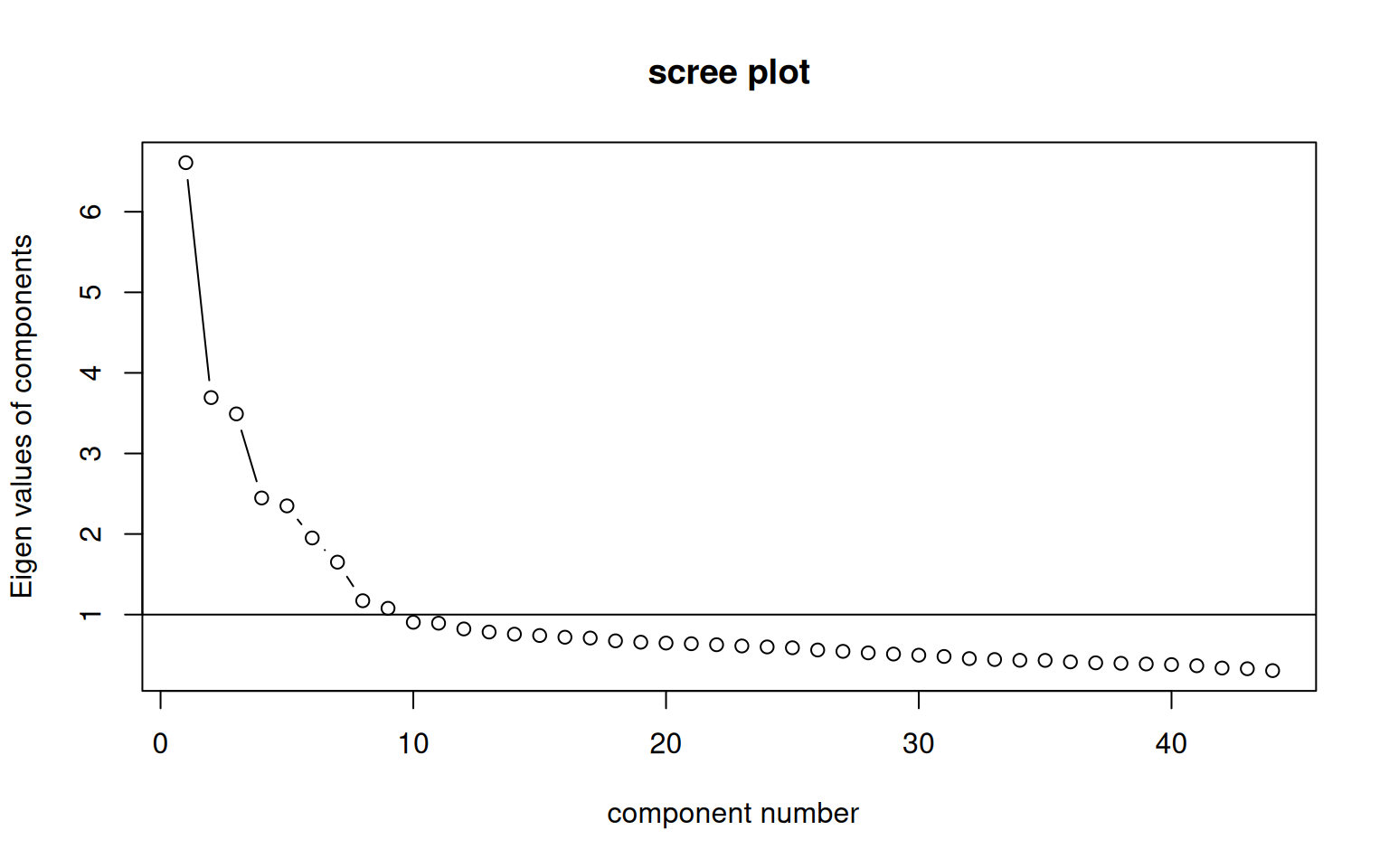

There are a number of approaches to picking the number of factors. As suggested by the VSS help file: > 1. Extracting factors until the chi square of the residual matrix is not significant. > 2. Extracting factors until the change in chi square from factor n to factor n+1 is not significant. > 3. Extracting factors until the eigen values of the real data are less than the corresponding eigen values of a random data set of the same size (parallel analysis) using fa.parallel. > 4. Plotting the magnitude of the successive eigen values and applying the scree test (a sudden drop in eigen values analogous to the change in slope seen when scrambling up the talus slope of a mountain and approaching the rock face. > 5. Extracting principal components until the eigen value < 1, and use that many factors. > 6. Extracting factors as long as they are interpetable. > 7. Using the Very Simple Structure Criterion (VSS). > 8. Using Wayne Velicer’s Minimum Average Partial (MAP) criterion.

The VSS function will display many of these criteria in a table. You can use any of these criteria, and we will look at many of them more specifically below. The output includes:

dof: degrees of freedom (if using FA)

chisq: chi square (from the factor analysis output (if using FA)

prob: probability of residual matrix > 0 (if using FA)

sqresid: squared residual correlations

RMSEA: the RMSEA for each number of factors

BIC: the BIC for each number of factors

eChiSq: the empirically found chi square

eRMS: Empirically found mean residual

eCRMS: Empirically found mean residual corrected for df

eBIC: The empirically found BIC based upon the eChiSq

fit: factor fit of the complete model

cfit.1: VSS fit of complexity 1

cfit.2: VSS fit of complexity 2

cfit.8: VSS fit of complexity 8

cresidiual.1: sum squared residual correlations for complexity 1

: sum squared residual correlations for complexity 2 ..8Running VSS requires giving it the raw correlation matrix:

Very Simple Structure

Call: vss(x = x, n = n, rotate = rotate, diagonal = diagonal, fm = fm,

n.obs = n.obs, plot = plot, title = title, use = use, cor = cor)

VSS complexity 1 achieves a maximimum of 0.52 with 6 factors

VSS complexity 2 achieves a maximimum of 0.67 with 5 factors

The Velicer MAP achieves a minimum of 0.01 with 7 factors

BIC achieves a minimum of -2977.51 with 8 factors

Sample Size adjusted BIC achieves a minimum of -1101.97 with 10 factors

Statistics by number of factors

vss1 vss2 map dof chisq prob sqresid fit RMSEA BIC SABIC complex eChisq

1 0.42 0.00 0.019 902 9845 0 59 0.42 0.100 3614 6479 1.0 25559

2 0.43 0.55 0.016 859 7801 0 46 0.55 0.090 1868 4596 1.4 17254

3 0.49 0.64 0.013 817 5617 0 34 0.67 0.077 -26 2568 1.5 9725

4 0.51 0.67 0.011 776 4260 0 28 0.72 0.067 -1101 1364 1.6 6604

SRMR eCRMS eBIC

1 0.116 0.119 19328

2 0.095 0.100 11320

3 0.072 0.077 4082

4 0.059 0.065 1244

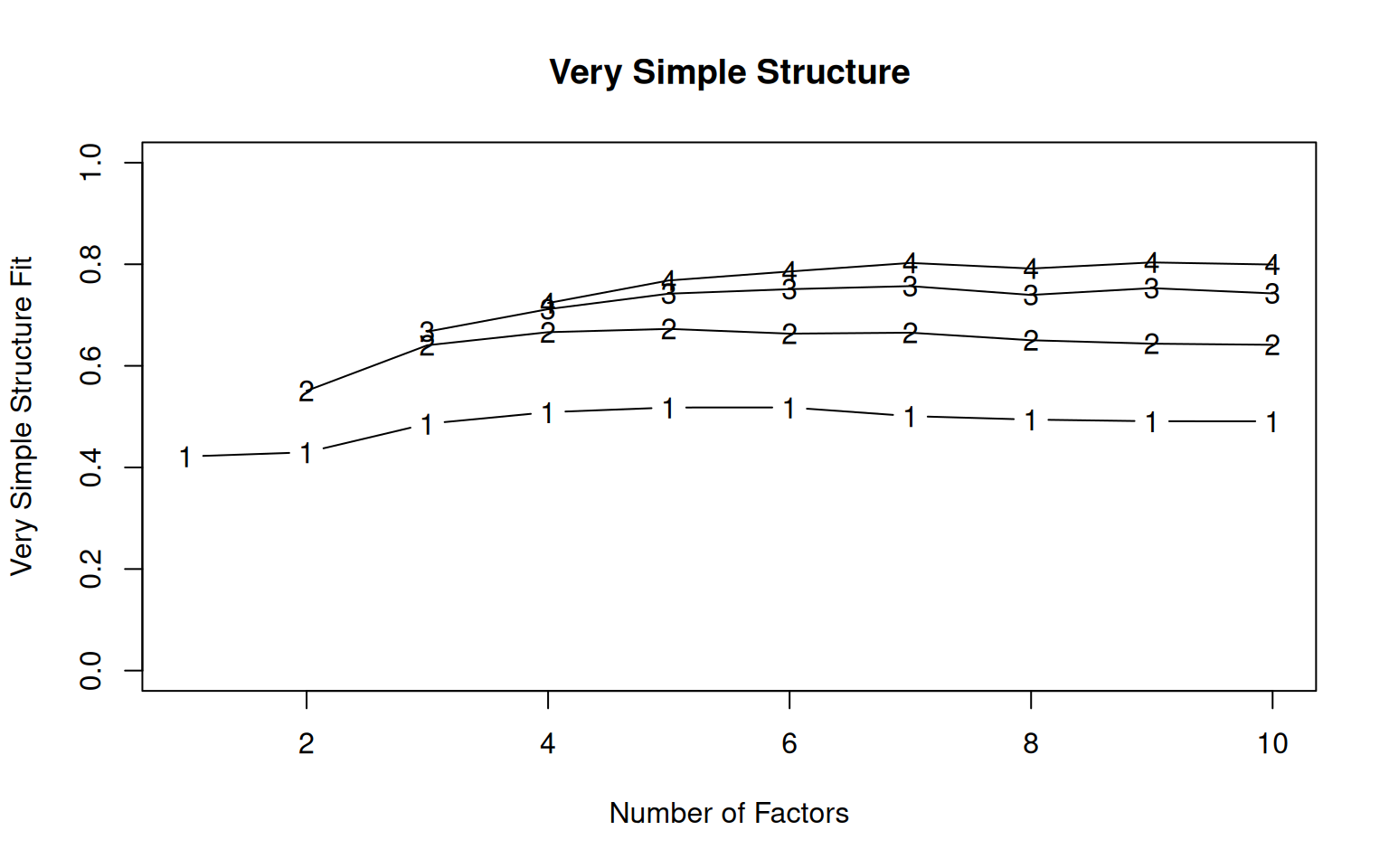

[ reached 'max' / getOption("max.print") -- omitted 6 rows ]These parallel lines are VSS statistics for reconstituting the correlation matrix with different numbers of simple factors, with the number indicating the complexity. VSS1 picks the largest value for each factor, VSS2 shows the two largest, etc. These two are shown numerically, and complexity 3 and 4 are also shown in the graph visually. The help suggests that these will peak at the optimal number of factors. Here, the output suggests the optimal is between 5 and 8, depending on your criterion.

Summary of goodness-of-fit statistics.

VSS

VSS scores tend to peak at a number of factors that is ‘most interpretable’. They compare the fit of the simplified model to the original correlations.

RMSEA

RMSEA score is a measure of root mean square error residuals. It says how far off you are, on average, when you compare the predicted correlation matrix and the actual one. Here, for 5 factors, it is .058, which is reasonably ‘good’, but not great (a RMSEA of .01 would be great). For 10 factors, it gets down to .028–but at what cost?

A RMSEA of .05 means that when you try to estimate the correlation matrix, each error is off by about .05.

TLI

TLI (Tucker-Lewis Index) is based on comparing expected versus observed chi-squared tests, penalizing by the size of the model. Here, it is .764 for 5 groups and .95 for 10 groups. A value of .9 is considered marginal, .95+ is good. So, 5 groups would be considered inadequate.

BIC and AIC

BIC is a relative measure, which combines goodness of fit in its likelihood with model complexity. Smaller or more negative scores are better. Here, BIC for 5-factor is -1919, and for 10-factor it is -2854.69. We need to be careful about interpreting BIC because sometimes functions report negative BIC. In this case, we are looking for the minimum BIC score, which occurs at 8 factors.

MAP: Velicer’s Minimal Average Partial

This will tend to minimize for the ‘best’ model.

Interpretability

More often than not, researchers rely on notions of interpretability to guide exploratory factor analysis. The statistics may tell you a ten-factor solution is needed, but you may only be able to interpret three. Ultimately, the goal of FA is usually scientific inference, and if the factor is not helping you understand anything, it might not be helpful to use.

Assessing general factors with the omega function

In intelligence research, factor analysis has often revealed a general intelligence element g that is general across all skills.

library(psych)

library(lavaan)

dat <- HolzingerSwineford1939[, 7:15]

colnames(dat) <- c("vis", "cubes", "lozenges", "pcomp", "scomp", "meaning", "addition",

"counting", "letters")

VSS(cor(dat), n = 5)

Very Simple Structure

Call: vss(x = x, n = n, rotate = rotate, diagonal = diagonal, fm = fm,

n.obs = n.obs, plot = plot, title = title, use = use, cor = cor)

VSS complexity 1 achieves a maximimum of 0.7 with 3 factors

VSS complexity 2 achieves a maximimum of 0.85 with 3 factors

The Velicer MAP achieves a minimum of 0.06 with 2 factors

BIC achieves a minimum of -22.87 with 4 factors

Sample Size adjusted BIC achieves a minimum of -3.81 with 4 factors

Statistics by number of factors

vss1 vss2 map dof chisq prob sqresid fit RMSEA BIC SABIC complex

1 0.61 0.00 0.080 27 1206 4.8e-237 6.4 0.61 0.209 1019.3 1105.1 1.0

2 0.65 0.76 0.063 19 436 1.7e-80 3.9 0.76 0.148 304.3 364.7 1.2

3 0.70 0.85 0.068 12 76 2.2e-11 2.1 0.87 0.073 -6.7 31.4 1.3

4 0.66 0.84 0.120 6 19 4.9e-03 1.8 0.89 0.046 -22.9 -3.8 1.4

eChisq SRMR eCRMS eBIC

1 1557.0 0.1471 0.170 1370

2 511.9 0.0843 0.116 381

3 26.1 0.0191 0.033 -57

4 5.5 0.0088 0.021 -36

[ reached 'max' / getOption("max.print") -- omitted 1 rows ]Principal Components Analysis

Call: principal(r = r, nfactors = nfactors, residuals = residuals,

rotate = rotate, n.obs = n.obs, covar = covar, scores = scores,

missing = missing, impute = impute, oblique.scores = oblique.scores,

method = method, use = use, cor = cor, correct = 0.5, weight = NULL)

Standardized loadings (pattern matrix) based upon correlation matrix

RC1 RC3 RC2 h2 u2 com

vis 0.32 0.67 0.17 0.59 0.41 1.6

cubes 0.08 0.73 -0.10 0.55 0.45 1.1

lozenges 0.02 0.78 0.15 0.63 0.37 1.1

pcomp 0.89 0.12 0.09 0.81 0.19 1.1

scomp 0.90 0.06 0.08 0.82 0.18 1.0

meaning 0.87 0.18 0.08 0.79 0.21 1.1

addition 0.10 -0.15 0.83 0.72 0.28 1.1

counting 0.04 0.14 0.82 0.69 0.31 1.1

letters 0.13 0.44 0.64 0.61 0.39 1.9

RC1 RC3 RC2

SS loadings 2.50 1.87 1.85

Proportion Var 0.28 0.21 0.21

Cumulative Var 0.28 0.49 0.69

Proportion Explained 0.40 0.30 0.30

Cumulative Proportion 0.40 0.70 1.00

Mean item complexity = 1.2

Test of the hypothesis that 3 components are sufficient.

The root mean square of the residuals (RMSR) is 0.08

Fit based upon off diagonal values = 0.93The default 3D pca of this data set shows three main factors with strong structure. The uniqueness suggests there is substantial error in each dimension not captured otherwise. How does FA do? Can we estimate a more general factor shared across all dimensions? Let’s try an EFA with both 3 and 4 dimensions. I will use varimax rotation to enforce orthogonal factors.

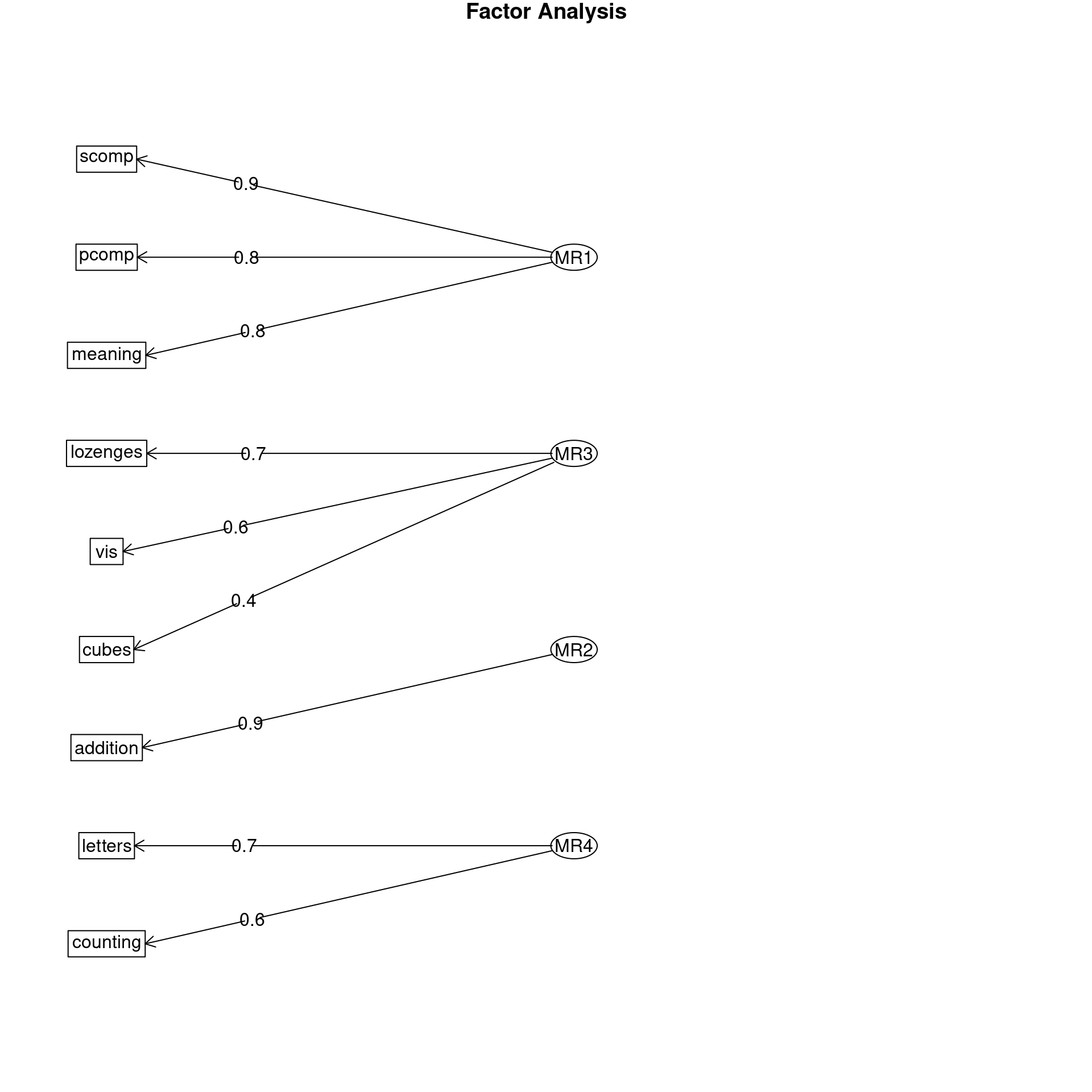

Factor Analysis using method = minres

Call: fa(r = dat, nfactors = 3, rotate = "varimax")

Standardized loadings (pattern matrix) based upon correlation matrix

MR1 MR3 MR2 h2 u2 com

vis 0.28 0.61 0.15 0.48 0.52 1.5

cubes 0.10 0.49 -0.03 0.26 0.74 1.1

lozenges 0.04 0.66 0.13 0.45 0.55 1.1

pcomp 0.83 0.16 0.10 0.73 0.27 1.1

scomp 0.86 0.09 0.09 0.75 0.25 1.0

meaning 0.80 0.21 0.09 0.69 0.31 1.2

addition 0.09 -0.08 0.71 0.52 0.48 1.1

counting 0.05 0.17 0.70 0.52 0.48 1.1

letters 0.13 0.41 0.52 0.46 0.54 2.0

MR1 MR3 MR2

SS loadings 2.19 1.34 1.33

Proportion Var 0.24 0.15 0.15

Cumulative Var 0.24 0.39 0.54

Proportion Explained 0.45 0.28 0.27

Cumulative Proportion 0.45 0.73 1.00

Mean item complexity = 1.3

Test of the hypothesis that 3 factors are sufficient.

df null model = 36 with the objective function = 3.05 with Chi Square = 904.1

df of the model are 12 and the objective function was 0.08

The root mean square of the residuals (RMSR) is 0.02

The df corrected root mean square of the residuals is 0.03

The harmonic n.obs is 301 with the empirical chi square 7.87 with prob < 0.8

The total n.obs was 301 with Likelihood Chi Square = 22.56 with prob < 0.032

Tucker Lewis Index of factoring reliability = 0.963

RMSEA index = 0.054 and the 90 % confidence intervals are 0.016 0.088

BIC = -45.93

Fit based upon off diagonal values = 1

Measures of factor score adequacy

MR1 MR3 MR2

Correlation of (regression) scores with factors 0.93 0.81 0.84

Multiple R square of scores with factors 0.87 0.66 0.70

Minimum correlation of possible factor scores 0.74 0.32 0.41Factor Analysis using method = minres

Call: fa(r = dat, nfactors = 4, rotate = "varimax")

Standardized loadings (pattern matrix) based upon correlation matrix

MR1 MR3 MR2 MR4 h2 u2 com

vis 0.29 0.56 0.00 0.24 0.45 0.5464 1.9

cubes 0.11 0.45 -0.09 0.09 0.23 0.7702 1.3

lozenges 0.03 0.73 0.09 0.11 0.55 0.4460 1.1

pcomp 0.83 0.18 0.11 0.03 0.74 0.2602 1.1

scomp 0.87 0.04 -0.03 0.16 0.79 0.2132 1.1

meaning 0.80 0.21 0.05 0.07 0.69 0.3133 1.2

addition 0.09 -0.07 0.93 0.36 1.00 0.0035 1.3

counting 0.06 0.13 0.32 0.55 0.42 0.5756 1.8

letters 0.13 0.33 0.13 0.65 0.57 0.4321 1.7

MR1 MR3 MR2 MR4

SS loadings 2.21 1.26 1.01 0.97

Proportion Var 0.25 0.14 0.11 0.11

Cumulative Var 0.25 0.39 0.50 0.60

Proportion Explained 0.41 0.23 0.18 0.18

Cumulative Proportion 0.41 0.64 0.82 1.00

Mean item complexity = 1.4

Test of the hypothesis that 4 factors are sufficient.

df null model = 36 with the objective function = 3.05 with Chi Square = 904.1

df of the model are 6 and the objective function was 0.02

The root mean square of the residuals (RMSR) is 0.01

The df corrected root mean square of the residuals is 0.02

The harmonic n.obs is 301 with the empirical chi square 1.66 with prob < 0.95

The total n.obs was 301 with Likelihood Chi Square = 5.49 with prob < 0.48

Tucker Lewis Index of factoring reliability = 1.004

RMSEA index = 0 and the 90 % confidence intervals are 0 0.071

BIC = -28.75

Fit based upon off diagonal values = 1

Measures of factor score adequacy

MR1 MR3 MR2 MR4

Correlation of (regression) scores with factors 0.94 0.82 0.96 0.74

Multiple R square of scores with factors 0.88 0.67 0.92 0.55

Minimum correlation of possible factor scores 0.76 0.34 0.84 0.10The FA with 3 finds a slightly different model, with letters fitting into visual more than speed–this was a task discriminating upper and lowercase letters, so maybe there is some truth to that. The factor analysis with 4 dimensions separates that into its own dimension. None of these capture a single common model, in order to estimate a ‘g’ factor.

A traditional version of the bifactor model is available in the omega

function in psych, which fits a general factor and then an

EFA on the residuals, and comparing the difference between these models.

This is more like EFA with a specific structure. The model implements a

factor analysis that fits one common factor and then unique

factors–attempting to identify the ‘g’ general factor that is commonly

found in intelligence research. Also, we discussed this model when

examining psychometrics: this is argued to be the best way to identify

whether a single factor exists, and more instructive than measures such

as cohen’s \(\alpha\) or GLB.

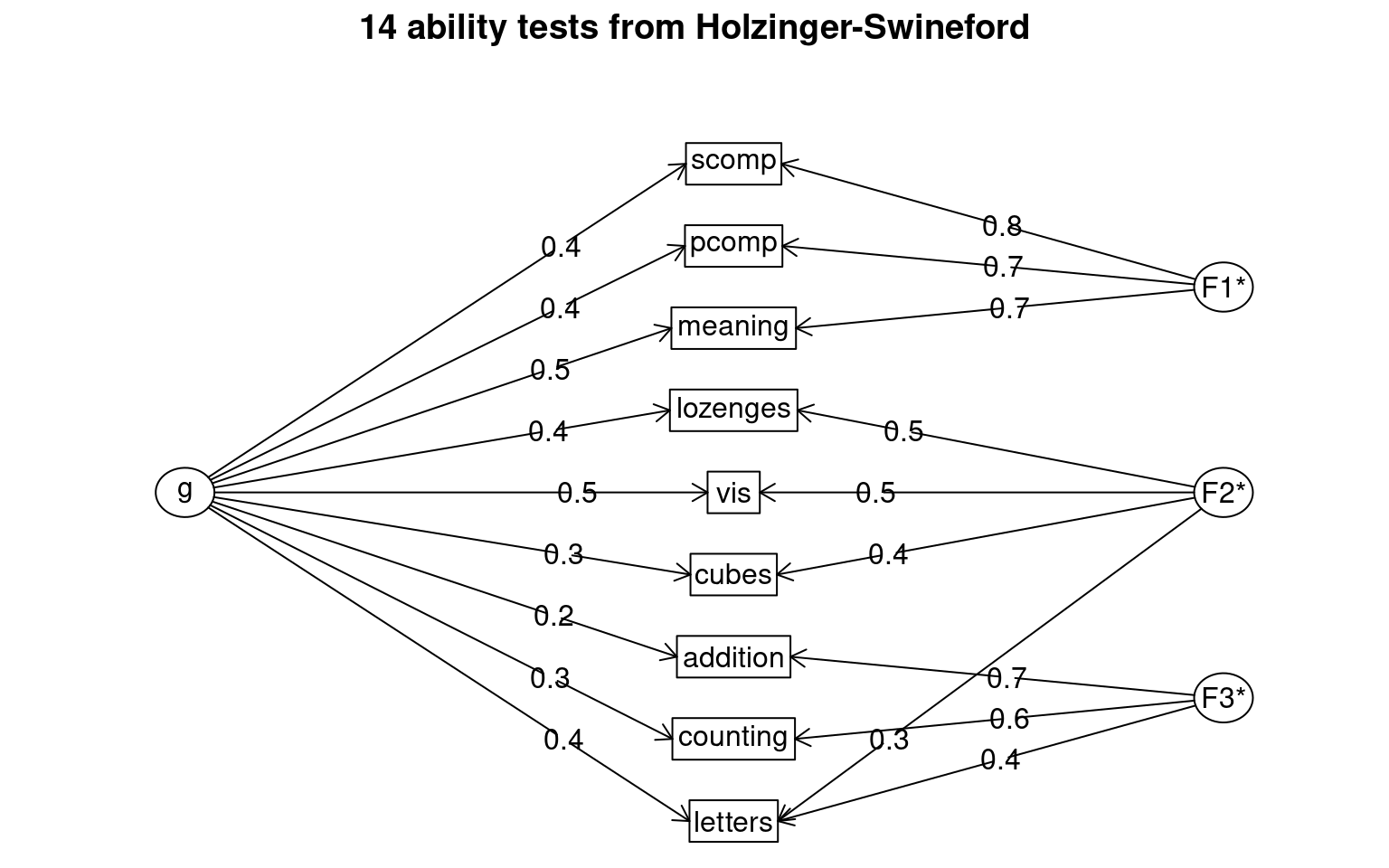

14 ability tests from Holzinger-Swineford

Call: omegah(m = m, nfactors = nfactors, fm = fm, key = key, flip = flip,

digits = digits, title = title, sl = sl, labels = labels,

plot = plot, n.obs = n.obs, rotate = rotate, Phi = Phi, option = option,

covar = covar)

Alpha: 0.76

G.6: 0.81

Omega Hierarchical: 0.45

Omega H asymptotic: 0.53

Omega Total 0.85

Schmid Leiman Factor loadings greater than 0.2

g F1* F2* F3* h2 u2 p2

vis 0.49 0.46 0.48 0.52 0.49

cubes 0.29 0.40 0.26 0.74 0.33

lozenges 0.41 0.53 0.45 0.55 0.37

pcomp 0.45 0.73 0.73 0.27 0.28

scomp 0.42 0.76 0.75 0.25 0.23

meaning 0.46 0.69 0.69 0.31 0.30

addition 0.23 0.67 0.52 0.48 0.10

counting 0.35 0.62 0.52 0.48 0.23

letters 0.45 0.30 0.42 0.46 0.54 0.43

With Sums of squares of:

g F1* F2* F3*

1.44 1.62 0.77 1.03

general/max 0.89 max/min = 2.09

mean percent general = 0.31 with sd = 0.12 and cv of 0.38

Explained Common Variance of the general factor = 0.3

The degrees of freedom are 12 and the fit is 0.08

The number of observations was 301 with Chi Square = 22.56 with prob < 0.032

The root mean square of the residuals is 0.02

The df corrected root mean square of the residuals is 0.03

RMSEA index = 0.054 and the 10 % confidence intervals are 0.016 0.088

BIC = -45.93

Compare this with the adequacy of just a general factor and no group factors

The degrees of freedom for just the general factor are 27 and the fit is 1.75

The number of observations was 301 with Chi Square = 517.02 with prob < 4.7e-92

The root mean square of the residuals is 0.2

The df corrected root mean square of the residuals is 0.23

RMSEA index = 0.246 and the 10 % confidence intervals are 0.228 0.265

BIC = 362.93

Measures of factor score adequacy

g F1* F2* F3*

Correlation of scores with factors 0.68 0.84 0.67 0.79

Multiple R square of scores with factors 0.46 0.71 0.45 0.62

Minimum correlation of factor score estimates -0.08 0.42 -0.10 0.23

Total, General and Subset omega for each subset

g F1* F2* F3*

Omega total for total scores and subscales 0.85 0.89 0.65 0.72

Omega general for total scores and subscales 0.45 0.24 0.27 0.19

Omega group for total scores and subscales 0.35 0.65 0.37 0.53Notice that the g factor is relatively strong here, and each of three factors load uniquely on a small subset of the other variables, and it also captures this ‘intermediate’ letter test. It also tests this complete model against the single group factor, so if the model fails, it suggests no more than one group is needed–that is, you have a coherent structure or a consensus. Thus, if that test fails, it may be the best approach to estimating a strong structure as an alternative to Cohen’s alpha–providing the first factor is sufficiently good.

We can try the ability.cov data as well using omega. 3 factors looks like it is too many, but a general factor is formed. 28% of the variance is accounted for by the common factor:

Omega

Call: omegah(m = m, nfactors = nfactors, fm = fm, key = key, flip = flip,

digits = digits, title = title, sl = sl, labels = labels,

plot = plot, n.obs = n.obs, rotate = rotate, Phi = Phi, option = option,

covar = covar)

Alpha: 0.86

G.6: 0.91

Omega Hierarchical: 0.4

Omega H asymptotic: 0.42

Omega Total 0.96

Schmid Leiman Factor loadings greater than 0.2

g F1* F2* h2 u2 p2

general 0.60 0.49 0.49 0.84 0.16 0.43

picture 0.47 0.78 0.83 0.17 0.26

blocks 0.53 0.88 1.05 -0.05 0.27

maze 0.34 0.65 0.56 0.44 0.21

reading 0.50 0.87 1.00 0.00 0.25

vocab 0.49 0.82 0.91 0.09 0.26

With Sums of squares of:

g F1* F2*

1.5 2.0 1.7

general/max 0.71 max/min = 1.23

mean percent general = 0.28 with sd = 0.08 and cv of 0.27

Explained Common Variance of the general factor = 0.28

The degrees of freedom are 4 and the fit is 19.35

The number of observations was 6 with Chi Square = 16.13 with prob < 0.0029

The root mean square of the residuals is 0.02

The df corrected root mean square of the residuals is 0.05

RMSEA index = 0.687 and the 10 % confidence intervals are 0.408 NA

BIC = 8.96

Compare this with the adequacy of just a general factor and no group factors

The degrees of freedom for just the general factor are 9 and the fit is 25.45

The number of observations was 6 with Chi Square = 38.18 with prob < 1.6e-05

The root mean square of the residuals is 0.4

The df corrected root mean square of the residuals is 0.51

RMSEA index = 0.712 and the 10 % confidence intervals are 0.552 NA

BIC = 22.06

Measures of factor score adequacy

g F1* F2*

Correlation of scores with factors 0.65 0.86 0.88

Multiple R square of scores with factors 0.42 0.74 0.77

Minimum correlation of factor score estimates -0.16 0.49 0.55

Total, General and Subset omega for each subset

g F1* F2*

Omega total for total scores and subscales 0.96 0.92 0.94

Omega general for total scores and subscales 0.40 0.23 0.33

Omega group for total scores and subscales 0.48 0.69 0.62

Omega

Call: omegah(m = m, nfactors = nfactors, fm = fm, key = key, flip = flip,

digits = digits, title = title, sl = sl, labels = labels,

plot = plot, n.obs = n.obs, rotate = rotate, Phi = Phi, option = option,

covar = covar)

Alpha: 0.86

G.6: 0.91

Omega Hierarchical: 0.65

Omega H asymptotic: 0.66

Omega Total 0.99

Schmid Leiman Factor loadings greater than 0.2

g F1* F2* F3* h2 u2 p2

general 0.71 0.57 0.84 0.16 0.60

picture 0.99 0.98 0.02 1.01

blocks 0.97 0.23 1.00 0.00 0.95

maze 0.65 0.76 1.00 0.00 0.42

reading 0.20 0.97 1.00 0.00 0.04

vocab 0.20 0.94 0.92 0.08 0.04

With Sums of squares of:

g F1* F2* F3*

2.93 2.16 0.00 0.63

general/max 1.36 max/min = Inf

mean percent general = 0.51 with sd = 0.42 and cv of 0.83

Explained Common Variance of the general factor = 0.51

The degrees of freedom are 0 and the fit is 17.39

The number of observations was 6 with Chi Square = 2.9 with prob < NA

The root mean square of the residuals is 0

The df corrected root mean square of the residuals is NA

Compare this with the adequacy of just a general factor and no group factors

The degrees of freedom for just the general factor are 9 and the fit is 23.53

The number of observations was 6 with Chi Square = 35.29 with prob < 5.3e-05

The root mean square of the residuals is 0.32

The df corrected root mean square of the residuals is 0.41

RMSEA index = 0.673 and the 10 % confidence intervals are 0.509 NA

BIC = 19.16

Measures of factor score adequacy

g F1* F2* F3*

Correlation of scores with factors 1.00 1.01 0 1.01

Multiple R square of scores with factors 1.00 1.01 0 1.01

Minimum correlation of factor score estimates 0.99 1.03 -1 1.02

Total, General and Subset omega for each subset

g F1* F2* F3*

Omega total for total scores and subscales 0.99 0.96 NA 0.99

Omega general for total scores and subscales 0.65 0.41 NA 0.73

Omega group for total scores and subscales 0.33 0.55 NA 0.27The bifactor model produced by omega includes a general

factor and then multiple additional unique factors. The interpretation

of these is a bit tricky–these might be thought of as the systematic

parts NOT included in the general factor. In this case, what are the

things that general intelligence, reading, and vocabulary share that

aren’t general intelligence? The interpretation is also tricky because

reading and vocab are relatively low in g, but high in F1.

Examining and displaying the models

It is common to display the results in several ways that show the factor structure. if you use the plot method, it will show you the points along each pair of dimensions, with point color-coded by whether they are high or low on each dimension. Looking at some of the FAs:

Example: Michigan House Votes

Use the Michigan house votes to compute a factor analysis. If necessary, determine what to do for ‘impute’, figure out how many factors to use, explore several rotations, and try to identify an interpretable result.

Assessing factors of political issues

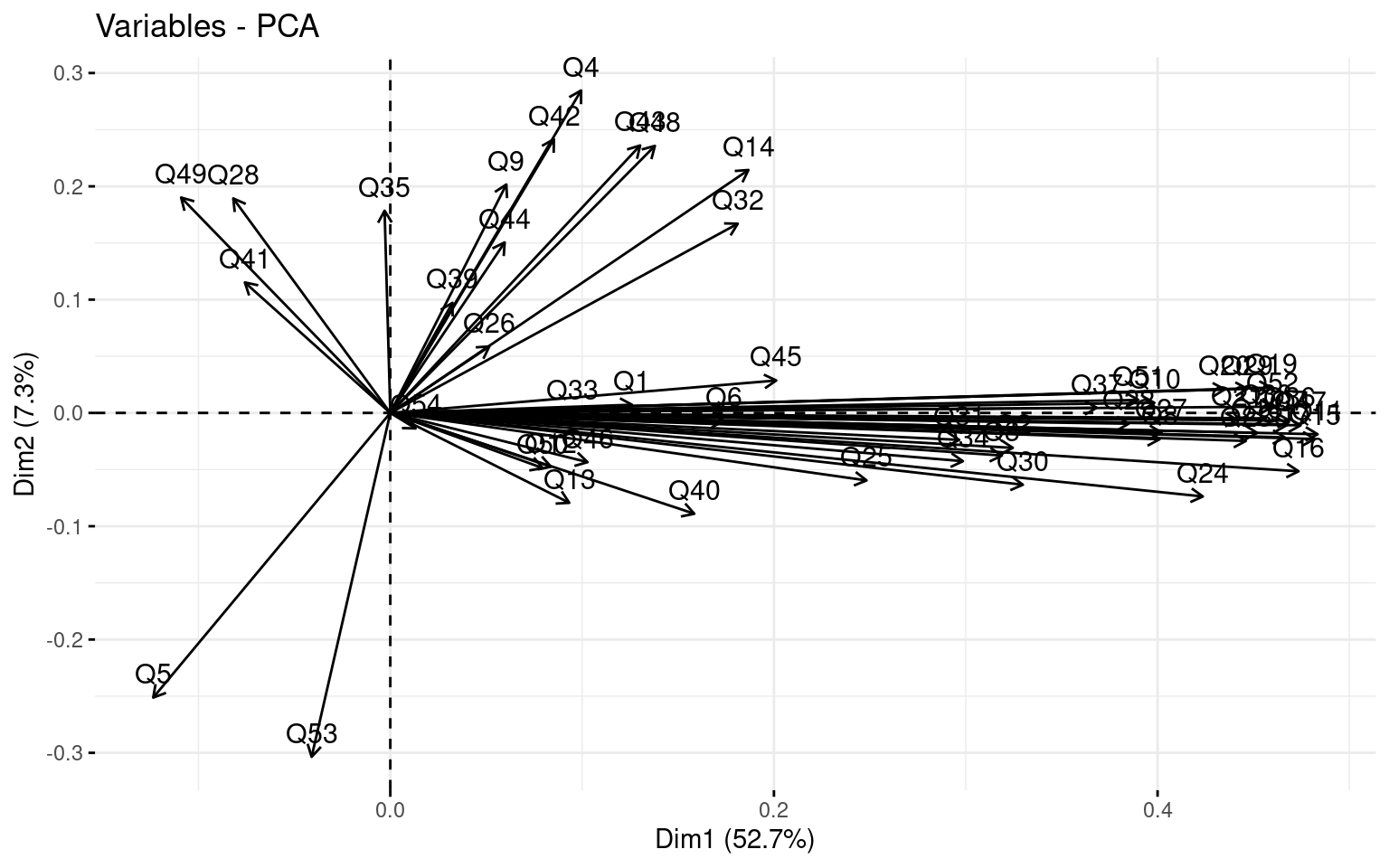

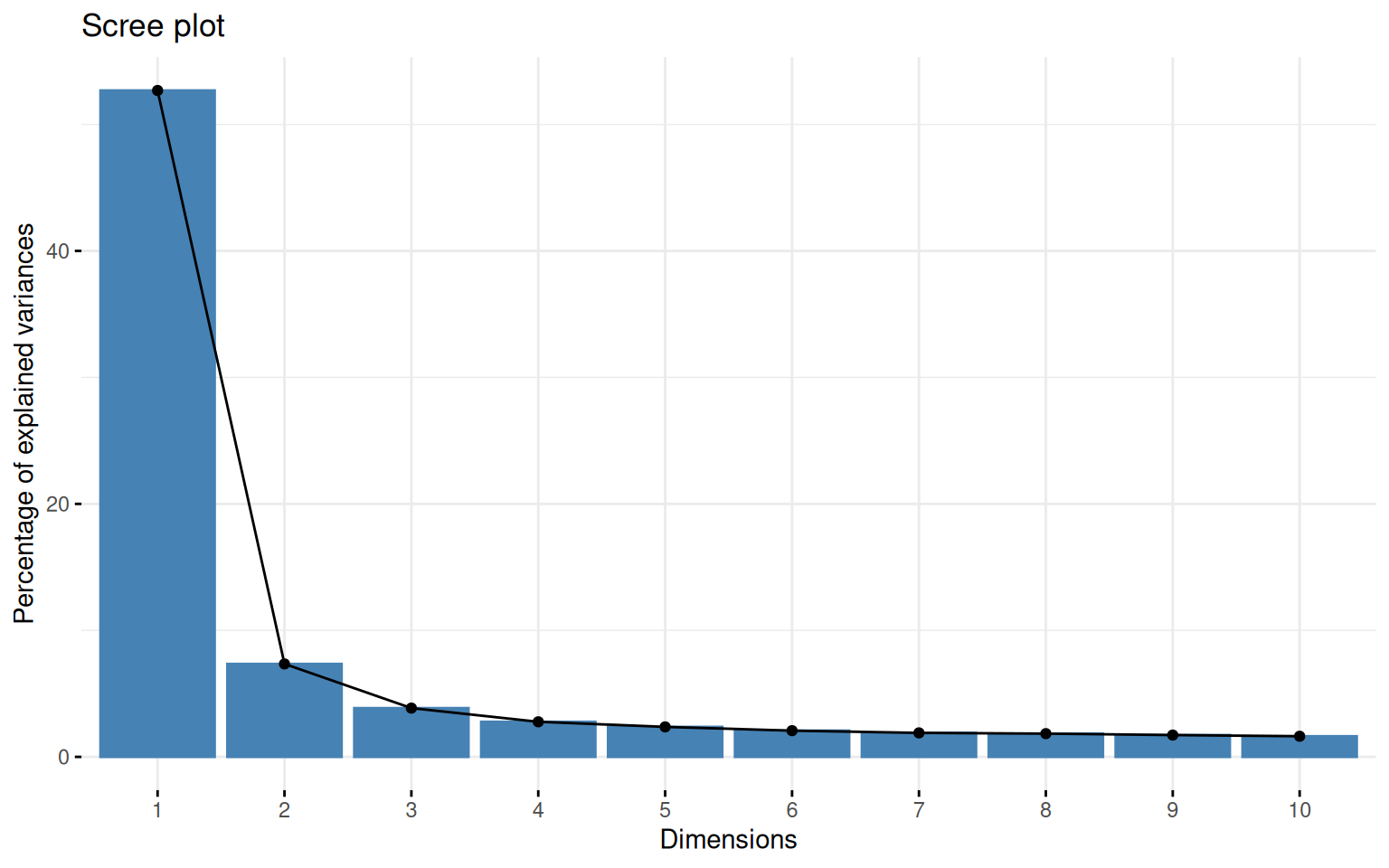

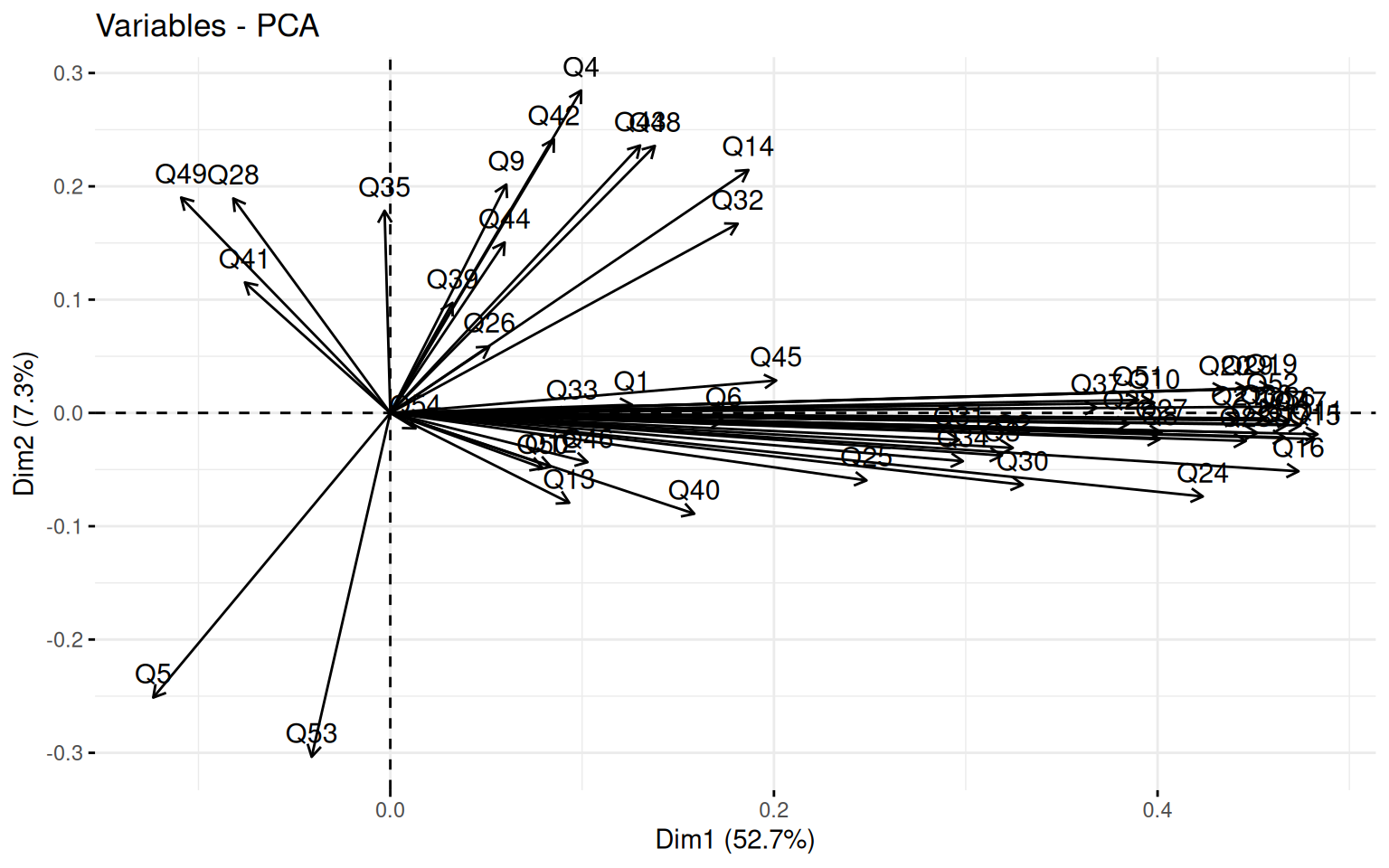

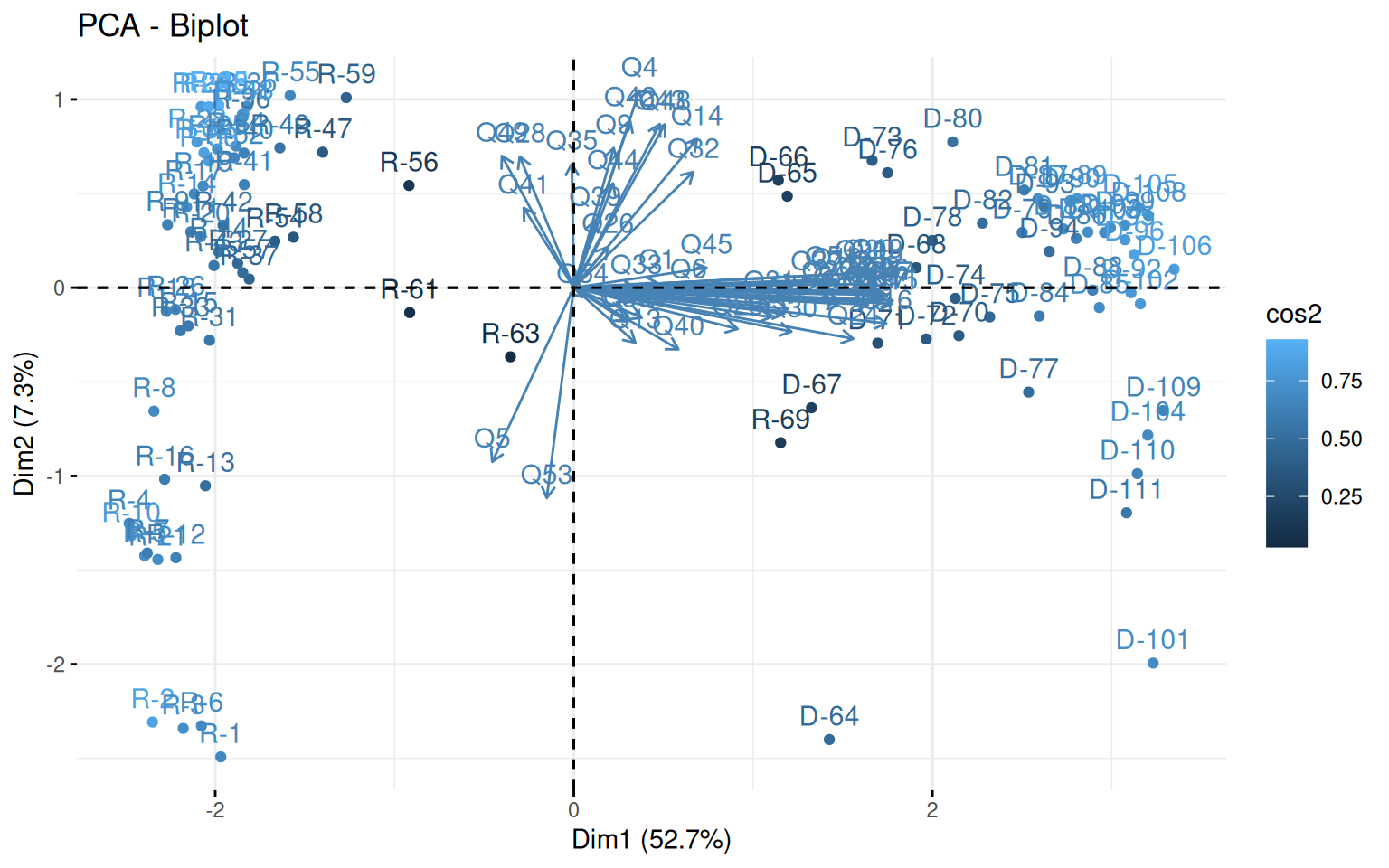

First we can look at a PCA to get an idea of the number of factors that might exist in the data. fvis_pca provides some interesting visualizations:

library(factoextra)

house <- read.csv("mihouse.csv")

votes <- house[, -(1:2)]

rownames(votes) <- paste(house$Party, 1:nrow(house), sep = "-")

pca <- princomp(~., data = votes, scores = T) #this handles NA values

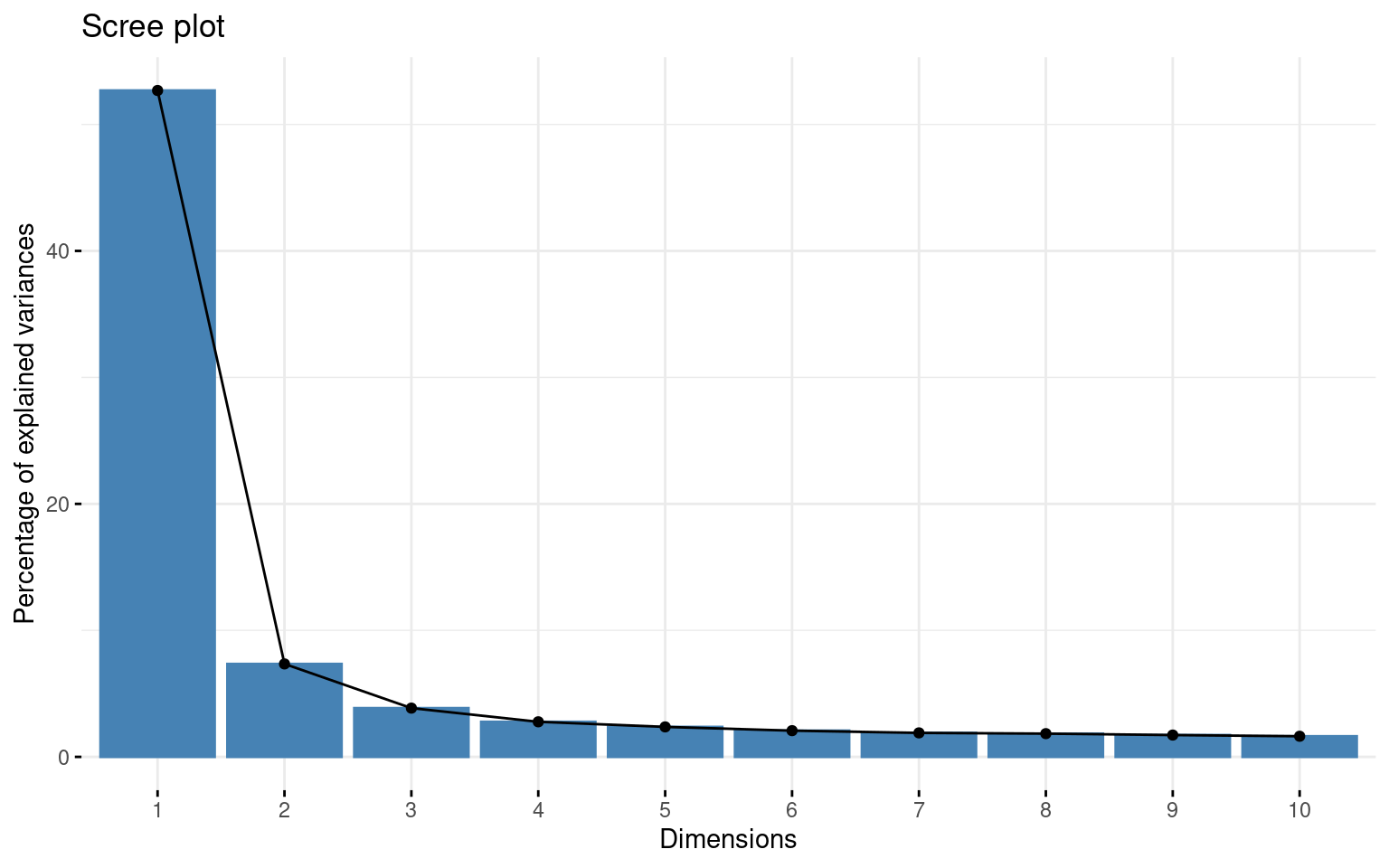

fviz_screeplot(pca)

Call:

princomp(formula = ~., data = votes, scores = T)

Standard deviations:

Comp.1 Comp.2 Comp.3 Comp.4 Comp.5 Comp.6 Comp.7

2.27298933 0.84883004 0.61473597 0.52132188 0.48197986 0.45073460 0.43112166

Comp.8 Comp.9 Comp.10 Comp.11 Comp.12 Comp.13 Comp.14

0.42431267 0.41106396 0.39977644 0.37296363 0.36746855 0.36208835 0.35478497

Comp.15 Comp.16 Comp.17 Comp.18 Comp.19 Comp.20 Comp.21

0.34330296 0.33065363 0.32432039 0.31664412 0.30303049 0.29492320 0.28551756

Comp.22 Comp.23 Comp.24 Comp.25 Comp.26 Comp.27 Comp.28

0.27993476 0.26451712 0.25354569 0.24797614 0.24107537 0.23097064 0.22455012

Comp.29 Comp.30 Comp.31 Comp.32 Comp.33 Comp.34 Comp.35

0.22218673 0.20988305 0.20171585 0.18798005 0.18474017 0.18368082 0.17029524

Comp.36 Comp.37 Comp.38 Comp.39 Comp.40 Comp.41 Comp.42

0.15998505 0.15194895 0.14373720 0.13993320 0.13420017 0.12630521 0.11776073

Comp.43 Comp.44 Comp.45 Comp.46 Comp.47 Comp.48 Comp.49

0.11428991 0.10488459 0.10316501 0.09802085 0.08799070 0.07692602 0.07392887

Comp.50 Comp.51 Comp.52 Comp.53 Comp.54

0.06341403 0.05926516 0.05214332 0.04332123 0.03207150

54 variables and 103 observations.

Loadings:

Comp.1 Comp.2 Comp.3 Comp.4 Comp.5 Comp.6 Comp.7 Comp.8 Comp.9 Comp.10

Q1 0.549 0.182 0.286 0.280 0.343 0.208

Comp.11 Comp.12 Comp.13 Comp.14 Comp.15 Comp.16 Comp.17 Comp.18 Comp.19

Q1 0.139 0.149 0.124 0.217 0.193

Comp.20 Comp.21 Comp.22 Comp.23 Comp.24 Comp.25 Comp.26 Comp.27 Comp.28

Q1 0.180 0.225 0.112 0.122

Comp.29 Comp.30 Comp.31 Comp.32 Comp.33 Comp.34 Comp.35 Comp.36 Comp.37

Q1 0.112

Comp.38 Comp.39 Comp.40 Comp.41 Comp.42 Comp.43 Comp.44 Comp.45 Comp.46

Q1

Comp.47 Comp.48 Comp.49 Comp.50 Comp.51 Comp.52 Comp.53 Comp.54

Q1

[ reached getOption("max.print") -- omitted 53 rows ]

Comp.1 Comp.2 Comp.3 Comp.4 Comp.5 Comp.6 Comp.7 Comp.8 Comp.9

SS loadings 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000

Comp.10 Comp.11 Comp.12 Comp.13 Comp.14 Comp.15 Comp.16 Comp.17

SS loadings 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000

Comp.18 Comp.19 Comp.20 Comp.21 Comp.22 Comp.23 Comp.24 Comp.25

SS loadings 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000

Comp.26 Comp.27 Comp.28 Comp.29 Comp.30 Comp.31 Comp.32 Comp.33

SS loadings 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000

Comp.34 Comp.35 Comp.36 Comp.37 Comp.38 Comp.39 Comp.40 Comp.41

SS loadings 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000

Comp.42 Comp.43 Comp.44 Comp.45 Comp.46 Comp.47 Comp.48 Comp.49

SS loadings 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000

Comp.50 Comp.51 Comp.52 Comp.53 Comp.54

SS loadings 1.000 1.000 1.000 1.000 1.000

[ reached getOption("max.print") -- omitted 2 rows ]Questions:

- How many factors seem reasonable?

- Looking at those factors, Can you make any interpretations?

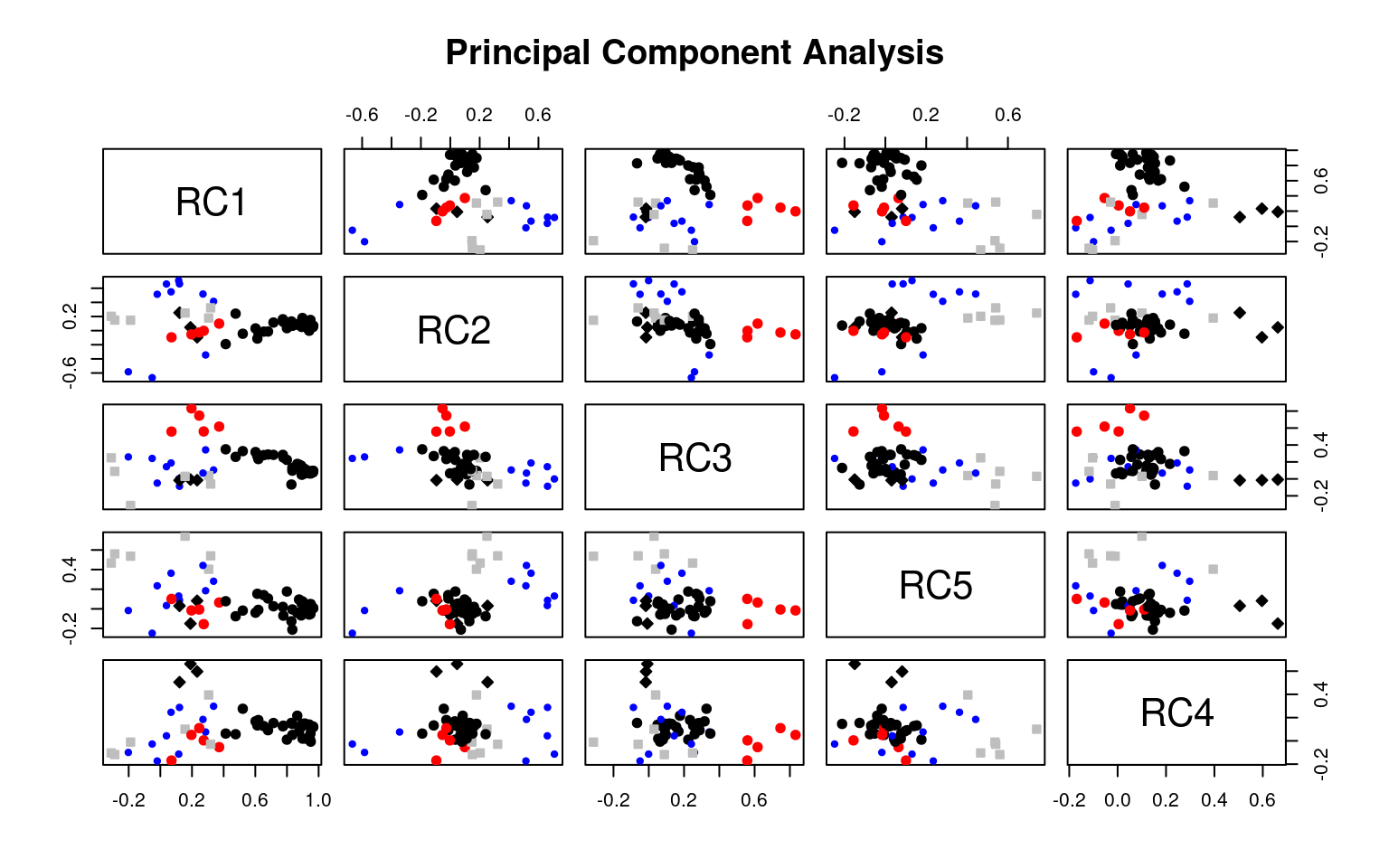

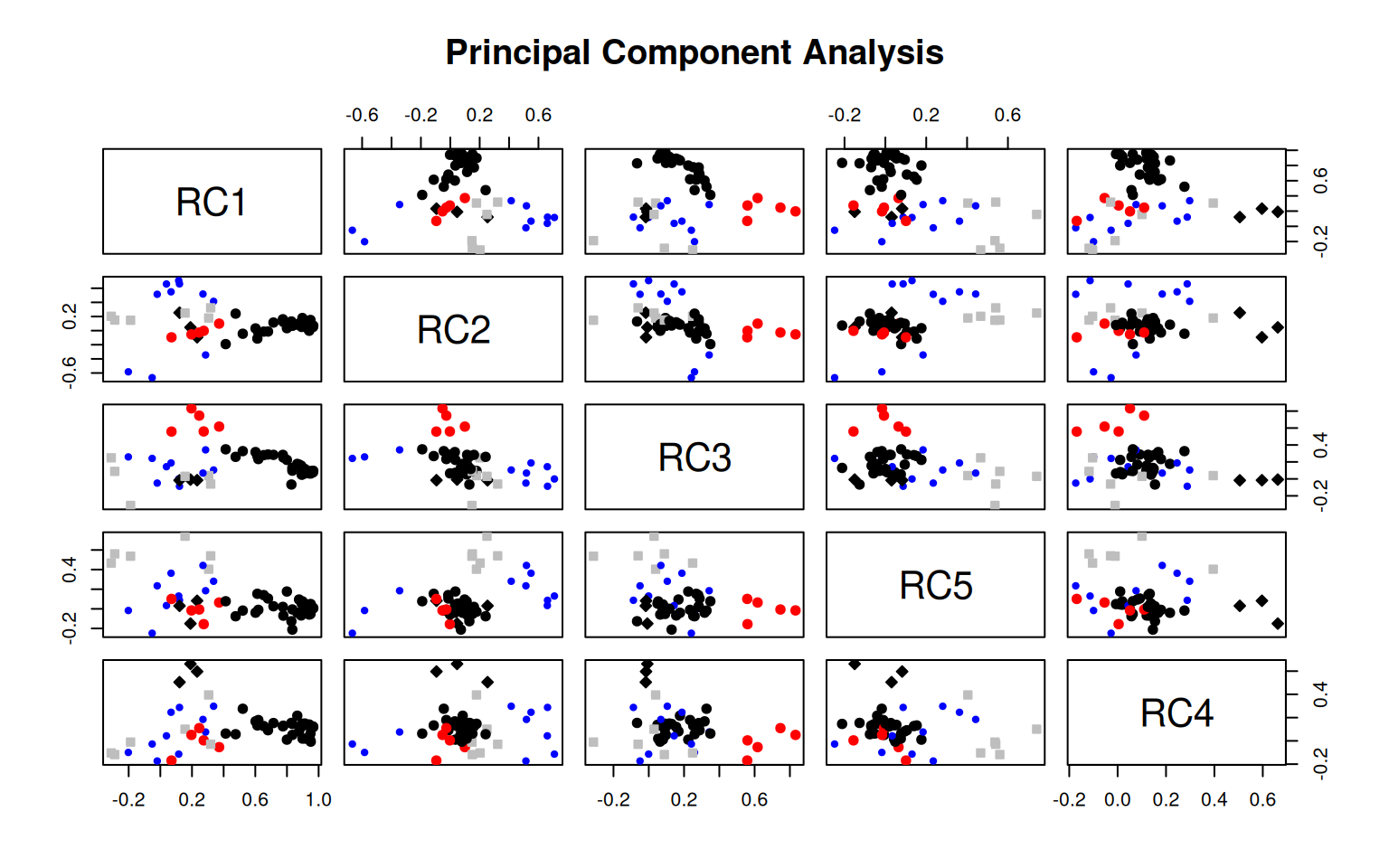

Try this with psych::principal, which will produce many of the same results as psych::fa

Principal Components Analysis

Call: psych::principal(r = votes, nfactors = 5)

Standardized loadings (pattern matrix) based upon correlation matrix

RC1 RC2 RC3 RC5 RC4 h2 u2 com

Q1 0.19 0.05 -0.01 -0.15 0.66 0.50 0.501 1.3

Q2 0.68 -0.01 0.29 0.11 0.09 0.57 0.435 1.4

Q3 0.61 -0.11 0.27 0.15 0.13 0.50 0.498 1.7

Q4 0.12 0.66 -0.09 0.09 0.29 0.55 0.449 1.5

Q5 -0.20 -0.58 0.26 -0.02 -0.10 0.46 0.541 1.7

Q6 0.37 0.10 0.62 0.06 -0.05 0.54 0.464 1.7

Q7 0.95 0.07 0.08 0.04 0.01 0.91 0.091 1.0

Q8 0.78 0.12 0.25 -0.07 0.13 0.70 0.295 1.3

Q9 0.12 0.71 0.00 0.13 -0.11 0.55 0.455 1.2

[ reached 'max' / getOption("max.print") -- omitted 45 rows ]

RC1 RC2 RC3 RC5 RC4

SS loadings 21.02 4.01 3.90 2.68 2.11

Proportion Var 0.39 0.07 0.07 0.05 0.04

Cumulative Var 0.39 0.46 0.54 0.59 0.62

Proportion Explained 0.62 0.12 0.12 0.08 0.06

Cumulative Proportion 0.62 0.74 0.86 0.94 1.00

Mean item complexity = 1.6

Test of the hypothesis that 5 components are sufficient.

The root mean square of the residuals (RMSR) is 0.05

with the empirical chi square 658.97 with prob < 1

Fit based upon off diagonal values = 0.99

Factor analysis:

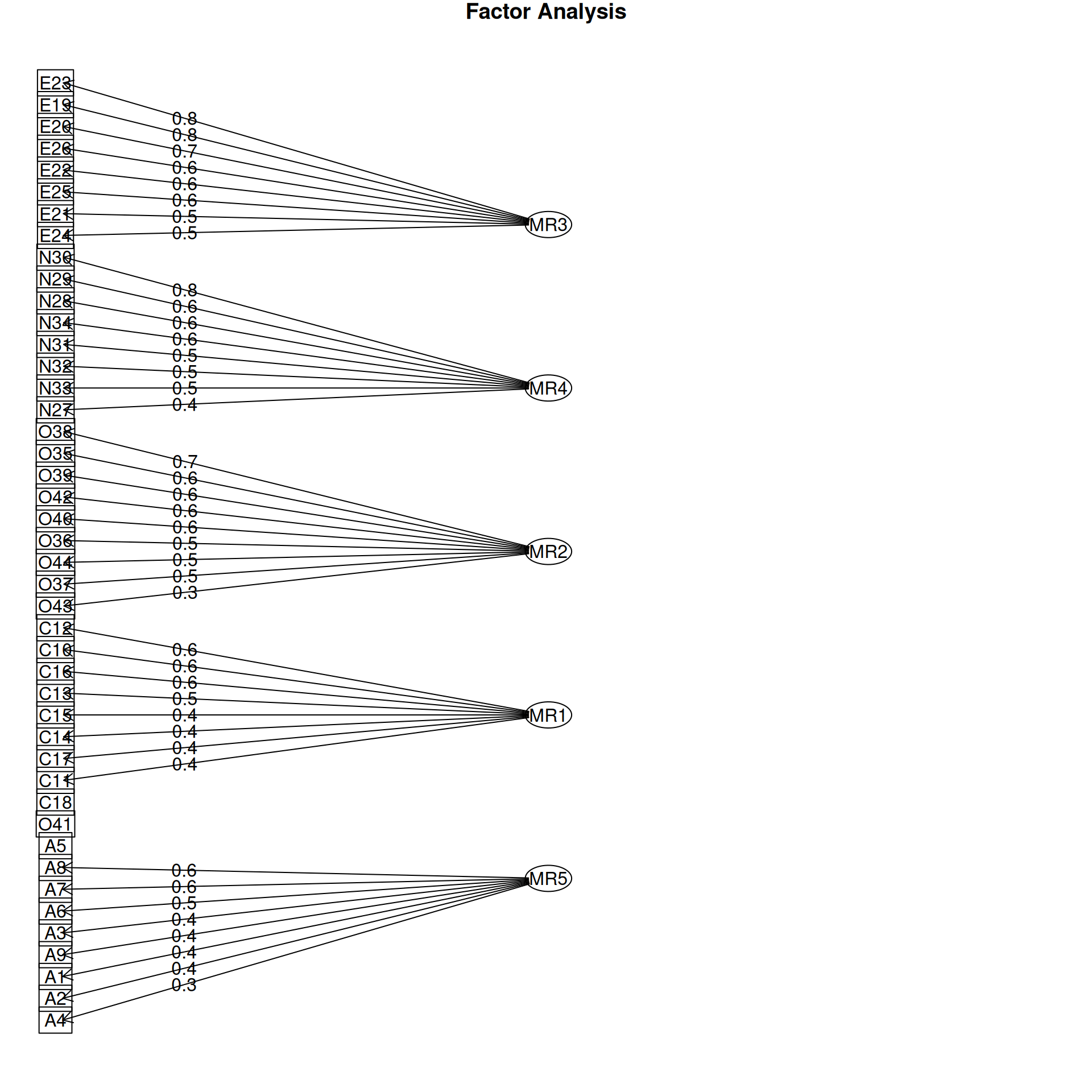

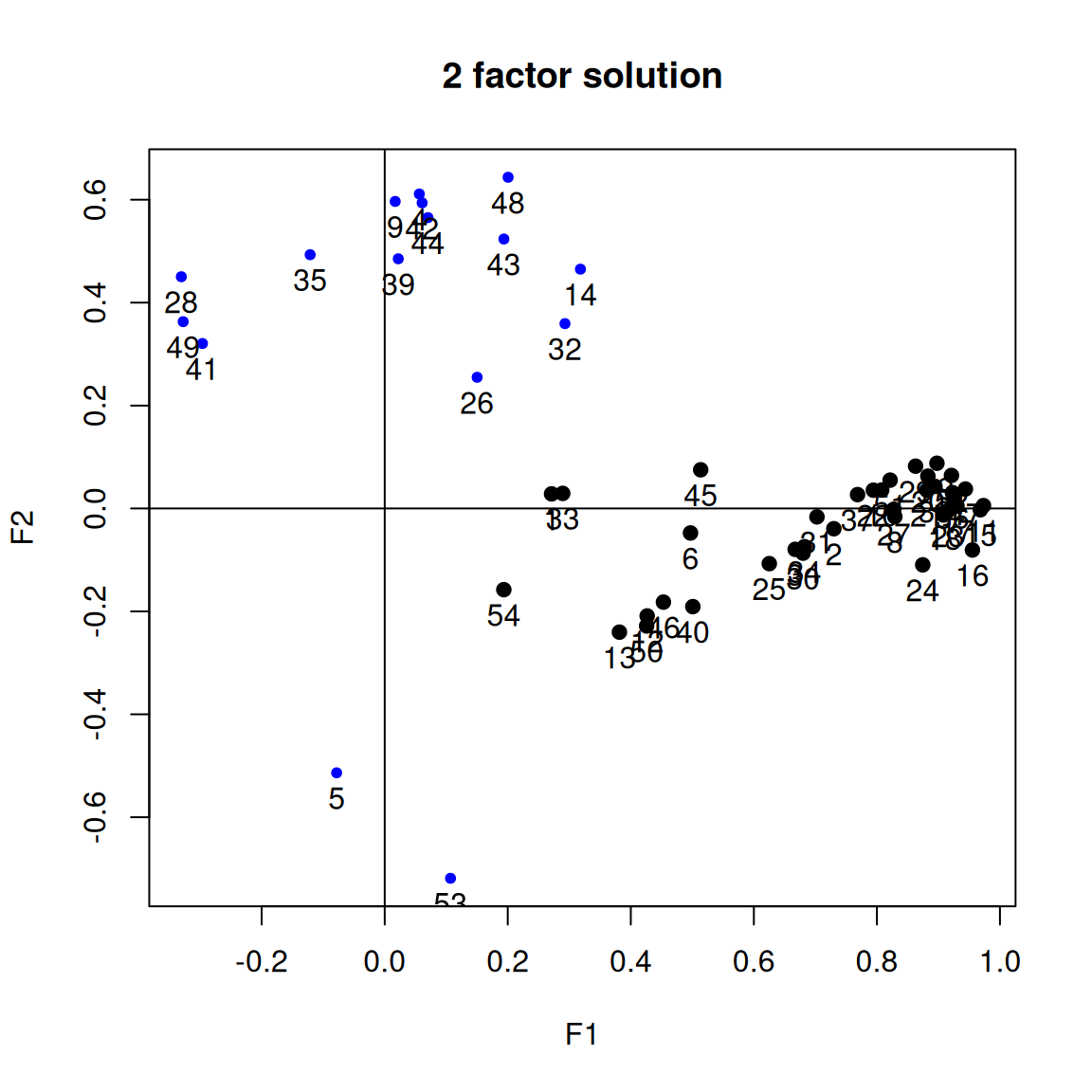

Perform a factor analysis with psych::fa. Determine how many dimensions are necessary, and justify model with goodness of fit parameters. - examine both orthogonal and non-orthogonal rotations - Create a plot showing the factor structure - examine models of different sizes to identify a good solution given the data set. - For the non-orthogonal rotation, examine correlations between factors.

Baseline solution:

efa5 <- psych::fa(r = votes, nfactors = 5)

efa5 <- psych::fa(r = votes, nfactors = 5, fm = "ols")

efa5Factor Analysis using method = ols

Call: psych::fa(r = votes, nfactors = 5, fm = "ols")

Standardized loadings (pattern matrix) based upon correlation matrix

1 2 3 4 5 h2 u2 com

Q1 0.14 -0.03 -0.14 0.41 -0.09 0.22 0.781 1.6

Q2 0.61 0.24 0.08 0.00 -0.04 0.55 0.455 1.3

Q3 0.52 0.19 0.17 0.07 -0.24 0.49 0.506 2.0

Q4 -0.01 -0.13 0.15 0.56 0.26 0.53 0.471 1.7

Q5 -0.20 0.27 -0.07 -0.26 -0.33 0.37 0.634 3.6

Q6 0.21 0.55 0.09 0.01 0.05 0.45 0.547 1.4

Q7 0.99 -0.03 0.07 -0.11 0.00 0.92 0.082 1.0

Q8 0.68 0.19 -0.08 0.16 0.03 0.70 0.300 1.3

Q9 0.12 0.04 0.07 -0.04 0.78 0.65 0.348 1.1

[ reached 'max' / getOption("max.print") -- omitted 45 rows ]

[,1] [,2] [,3] [,4] [,5]

SS loadings 20.55 3.67 2.65 2.30 2.23

Proportion Var 0.38 0.07 0.05 0.04 0.04

Cumulative Var 0.38 0.45 0.50 0.54 0.58

Proportion Explained 0.65 0.12 0.08 0.07 0.07

Cumulative Proportion 0.65 0.77 0.86 0.93 1.00

With factor correlations of

[,1] [,2] [,3] [,4] [,5]

[1,] 1.00 0.37 0.10 0.38 0.06

[2,] 0.37 1.00 0.06 0.12 -0.14

[3,] 0.10 0.06 1.00 0.17 0.29

[4,] 0.38 0.12 0.17 1.00 0.22

[5,] 0.06 -0.14 0.29 0.22 1.00

Mean item complexity = 1.7

Test of the hypothesis that 5 factors are sufficient.

df null model = 1431 with the objective function = 88.41 with Chi Square = 8148.49

df of the model are 1171 and the objective function was 38.21

The root mean square of the residuals (RMSR) is 0.04

The df corrected root mean square of the residuals is 0.04

The harmonic n.obs is 106 with the empirical chi square 469.15 with prob < 1

The total n.obs was 112 with Likelihood Chi Square = 3394.07 with prob < 6.3e-215

Tucker Lewis Index of factoring reliability = 0.577

RMSEA index = 0.13 and the 90 % confidence intervals are 0.126 0.136

BIC = -2131.29

Fit based upon off diagonal values = 0.99

Measures of factor score adequacy

[,1] [,2] [,3] [,4] [,5]

Correlation of (regression) scores with factors 1 0.95 0.93 0.90 0.91

Multiple R square of scores with factors 1 0.91 0.87 0.81 0.83

Minimum correlation of possible factor scores 1 0.81 0.73 0.62 0.65Overall, the fit is not great (RMSEA =.13, TL=.577). These don’t change appreciably as we change the size of the model, so it indicates that the data are not well described by a factor-space model.

Factor Analysis using method = ols

Call: psych::fa(r = votes, nfactors = 9, fm = "ols")

Standardized loadings (pattern matrix) based upon correlation matrix

1 2 3 4 5 6 7 8 9 h2 u2 com

Q1 -0.03 -0.07 0.12 0.54 -0.06 -0.02 0.03 -0.02 0.12 0.32 0.68 1.3

Q2 0.36 0.15 0.04 0.06 0.01 0.03 0.37 0.14 0.05 0.62 0.38 2.8

Q3 0.41 0.18 0.03 0.10 0.13 -0.17 0.07 0.16 0.08 0.49 0.51 2.8

Q4 -0.16 -0.02 0.73 0.10 -0.09 0.16 0.01 0.05 0.08 0.60 0.40 1.3

Q5 -0.28 0.08 -0.46 0.13 0.09 -0.17 0.13 0.21 -0.12 0.44 0.56 3.2

Q6 0.06 0.47 0.03 -0.01 0.04 0.11 0.13 0.27 -0.03 0.49 0.51 2.0

[ reached 'max' / getOption("max.print") -- omitted 48 rows ]

[,1] [,2] [,3] [,4] [,5] [,6] [,7] [,8] [,9]

SS loadings 17.84 3.42 3.10 2.13 2.07 1.93 1.76 1.74 0.76

Proportion Var 0.33 0.06 0.06 0.04 0.04 0.04 0.03 0.03 0.01

Cumulative Var 0.33 0.39 0.45 0.49 0.53 0.56 0.60 0.63 0.64

Proportion Explained 0.51 0.10 0.09 0.06 0.06 0.06 0.05 0.05 0.02

Cumulative Proportion 0.51 0.61 0.70 0.76 0.82 0.88 0.93 0.98 1.00

With factor correlations of

[,1] [,2] [,3] [,4] [,5] [,6] [,7] [,8] [,9]

[1,] 1.00 0.35 0.33 0.45 0.00 0.10 0.41 0.40 0.07

[2,] 0.35 1.00 -0.01 0.24 0.07 -0.03 0.29 0.27 -0.02

[3,] 0.33 -0.01 1.00 0.13 0.25 0.37 0.09 0.12 0.11

[4,] 0.45 0.24 0.13 1.00 -0.08 0.04 0.14 0.17 0.04

[5,] 0.00 0.07 0.25 -0.08 1.00 0.22 0.00 0.02 0.02

[6,] 0.10 -0.03 0.37 0.04 0.22 1.00 -0.04 -0.01 0.08

[7,] 0.41 0.29 0.09 0.14 0.00 -0.04 1.00 0.16 -0.01

[8,] 0.40 0.27 0.12 0.17 0.02 -0.01 0.16 1.00 0.02

[ reached getOption("max.print") -- omitted 1 row ]

Mean item complexity = 2.2

Test of the hypothesis that 9 factors are sufficient.

df null model = 1431 with the objective function = 88.41 with Chi Square = 8148.49

df of the model are 981 and the objective function was 34.58

The root mean square of the residuals (RMSR) is 0.03

The df corrected root mean square of the residuals is 0.04

The harmonic n.obs is 106 with the empirical chi square 258.06 with prob < 1

The total n.obs was 112 with Likelihood Chi Square = 2979.39 with prob < 4.4e-200

Tucker Lewis Index of factoring reliability = 0.529

RMSEA index = 0.135 and the 90 % confidence intervals are 0.13 0.141

BIC = -1649.46

Fit based upon off diagonal values = 1

Measures of factor score adequacy

[,1] [,2] [,3] [,4] [,5] [,6]

Correlation of (regression) scores with factors 1 0.95 0.93 0.93 0.91 0.91

Multiple R square of scores with factors 1 0.90 0.86 0.86 0.82 0.83

Minimum correlation of possible factor scores 1 0.80 0.72 0.71 0.65 0.66

[,7] [,8] [,9]

Correlation of (regression) scores with factors 0.89 0.91 0.86

Multiple R square of scores with factors 0.80 0.83 0.74

Minimum correlation of possible factor scores 0.59 0.65 0.49Here, with 9 factors, the BIC gets appreciable worse.

Factor Analysis using method = ols

Call: psych::fa(r = votes, nfactors = 2, fm = "ols")

Standardized loadings (pattern matrix) based upon correlation matrix

1 2 h2 u2 com

Q1 0.27 0.03 0.078 0.922 1.0

Q2 0.73 -0.04 0.521 0.479 1.0

Q3 0.67 -0.08 0.427 0.573 1.0

Q4 0.06 0.61 0.393 0.607 1.0

Q5 -0.08 -0.51 0.289 0.711 1.0

Q6 0.50 -0.05 0.238 0.762 1.0

Q7 0.93 0.02 0.869 0.131 1.0

Q8 0.83 -0.02 0.682 0.318 1.0

Q9 0.02 0.60 0.361 0.639 1.0

Q10 0.81 0.04 0.667 0.333 1.0

Q11 0.97 0.01 0.950 0.050 1.0

Q12 0.43 -0.21 0.184 0.816 1.5

Q13 0.38 -0.24 0.161 0.839 1.7

Q14 0.32 0.47 0.386 0.614 1.8

Q15 0.97 0.00 0.936 0.064 1.0

[ reached 'max' / getOption("max.print") -- omitted 39 rows ]

[,1] [,2]

SS loadings 22.42 4.50

Proportion Var 0.42 0.08

Cumulative Var 0.42 0.50

Proportion Explained 0.83 0.17

Cumulative Proportion 0.83 1.00

With factor correlations of

[,1] [,2]

[1,] 1.00 0.23

[2,] 0.23 1.00

Mean item complexity = 1.2

Test of the hypothesis that 2 factors are sufficient.

df null model = 1431 with the objective function = 88.41 with Chi Square = 8148.49

df of the model are 1324 and the objective function was 44.05

The root mean square of the residuals (RMSR) is 0.06

The df corrected root mean square of the residuals is 0.07

The harmonic n.obs is 106 with the empirical chi square 1193.18 with prob < 1

The total n.obs was 112 with Likelihood Chi Square = 4001.64 with prob < 2.7e-266